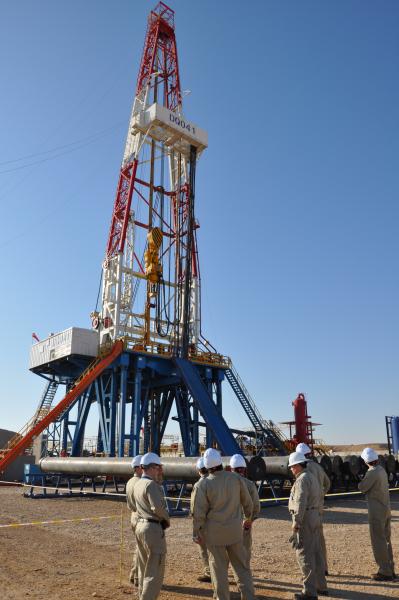

Production drilling for oil. Oil drilling process

Drilling is the impact of special equipment on the soil layers, as a result of which a well is formed in the ground, through which valuable resources will be extracted. The process of drilling oil wells is carried out in different areas of work, which depend on the location of the soil or mountain formation: it can be horizontal, vertical or inclined.

As a result of work, a cylindrical void is formed in the ground in the form of a straight shaft, or well. Its diameter may vary depending on the purpose, but it is always less than the length parameter. The beginning of the well is located on the soil surface. The walls are called the trunk, and the bottom of the well is called the bottom.

Key milestones

If medium and light equipment can be used for water wells, then only heavy equipment can be used for oil well drilling. The drilling process can only be carried out with the help of special equipment.

The process itself is divided into the following stages:

- Delivery of equipment to the site where the work will be done.

- The actual drilling of the mine. The process includes several works, one of which is the deepening of the shaft, which occurs with the help of regular flushing and further destruction of the rock.

- So that the wellbore is not destroyed and does not clog it, the rock layers are strengthened. For this purpose, a special column of interconnected pipes is laid in space. The place between the pipe and the rock is fixed with cement mortar: this work is called plugging.

- The last work is development. The last layer of rock is opened on it, a bottomhole zone is formed, and the mine is perforated and fluid is drained.

Site preparation

To organize the process of drilling an oil well, it will also be necessary to carry out preparatory stage. If the development is carried out in the forest area, it is required, in addition to the preparation of the main documentation, to obtain consent to work in the forestry. The preparation of the site itself includes the following steps:

- Cutting down trees in the area.

- The division of the zone into separate parts of the earth.

- Drawing up a work plan.

- Establishment of a settlement to house the labor force.

- Ground preparation for the drilling station.

- Carrying out marking at the place of work.

- Creation of foundations for the installation of tanks in a warehouse with combustible materials.

- Arrangement of warehouses, delivery and debugging of equipment.

After that, it is necessary to start preparing equipment directly for drilling oil wells. This stage includes the following processes:

- Installation and testing of equipment.

- Wiring lines for power supply.

- Installation of bases and auxiliary elements for the tower.

- Installing the tower and lifting to the desired height.

- Debugging of all equipment.

When the oil drilling equipment is ready for operation, it is necessary to obtain a conclusion from a special commission that the equipment is in good condition and ready for work, and the personnel have sufficient knowledge in the field of safety rules in this kind of production. When checking, it is clarified whether lighting devices have the correct design (they must have an explosion-resistant casing), whether lighting with a voltage of 12V is installed along the depth of the mine. Notes regarding the quality of work and safety must be taken into account in advance.

Prior to drilling a well, it is necessary to install a hole, bring in pipes to strengthen the drill shaft, a chisel, small special equipment for auxiliary work, casing pipes, instruments for measuring during drilling, provide water supply and resolve other issues.

The drilling site contains accommodation facilities for workers, technical facilities, a laboratory building for analysis of soil samples and the results obtained, warehouses for inventory and small working tools, as well as medical aid and safety facilities.

Features of drilling an oil well

After installation, the processes of re-equipment of the traveling system begin: in the course of these works, equipment is installed, and small mechanical means are also tested. Installation of the mast opens the process of drilling into the soil; the direction should not diverge from the axial center of the tower.

After the centering is completed, a well is created for the direction: this process means installing a pipe to strengthen the wellbore and pouring the initial part with cement. After setting the direction, the centering between the tower itself and the rotary axes is re-adjusted.

Pit drilling is carried out in the center of the shaft, and in the process, casing is made using pipes. When drilling a hole, a turbodrill is used; to adjust the rotation speed, it is necessary to hold it with a rope, which is fixed on the tower itself, and is physically held by the other part.

A couple of days before the launch of the drilling rig, when the preparatory stage has passed, a conference is held with the participation of members of the administration: technologists, geologists, engineers, drillers. The issues discussed at the conference include the following:

- Diagram of bedding on oil field: a layer of clay, a layer of sandstone with water carriers, a layer of oil deposits.

- Design features of the well.

- The composition of the rock at the point of research and development.

- Accounting possible difficulties and complicating factors that may occur when drilling an oil well in a particular case.

- Consideration and analysis of the map of standards.

- Consideration of issues related to trouble-free wiring.

Documents and equipment: basic requirements

The process of drilling a well for oil can begin only after a number of documents have been issued. These include the following:

- Permission to start the operation of the drilling site.

- Map of standards.

- Journal of drilling fluids.

- Journal of Occupational Safety at Work.

- Accounting for the functioning of diesel engines.

- Watch log.

To the main mechanical equipment and consumables that are used in the process of drilling a well, include the following types:

- Cementing equipment, cement mortar itself.

- Safety equipment.

- Logging mechanisms.

- Technical water.

- Reagents for various purposes.

- Water for drinking.

- Pipes for casing and actual drilling.

- Helicopter pad.

Well types

In the process of drilling an oil well, a mine is formed in the rock, which is checked for the presence of oil or gas by perforating the wellbore, which stimulates the inflow of the desired substance from the productive area. After that, the drilling equipment is dismantled, the well is sealed with the start and end dates of drilling, and then the debris is removed, and the metal parts are recycled.

In the process of drilling an oil well, a mine is formed in the rock, which is checked for the presence of oil or gas by perforating the wellbore, which stimulates the inflow of the desired substance from the productive area. After that, the drilling equipment is dismantled, the well is sealed with the start and end dates of drilling, and then the debris is removed, and the metal parts are recycled. At the beginning of the process, the diameter of the trunk is up to 90 cm, and by the end it rarely reaches 16.5 cm. In the course of work, the construction of a well is done in several stages:

- The deepening of the day of the well, for which drilling equipment is used: it crushes the rock.

- Removal of debris from the mine.

- Fixing the trunk with pipes and cement.

- Works during which the obtained fault is investigated, productive locations of oil are revealed.

- Descent of depth and its cementing.

Wells can vary in depth and are divided into the following varieties:

- Small (up to 1500 meters).

- Medium (up to 4500 meters).

- Deep (up to 6000 meters).

- Super deep (more than 6000 meters).

Drilling a well involves crushing an entire rock formation with a chisel. The resulting parts are removed by washing with a special solution; the depth of the mine becomes greater when the entire bottomhole area is destroyed.

Problems during oil drilling

During the drilling of wells, a number of technical problems can be encountered that will slow down or make work almost impossible. These include the following events:

- The destruction of the trunk, landslides.

- Departure into the soil of a liquid for washing (removal of parts of the rock).

- Emergency conditions of equipment or mine.

- Drilling errors.

Most often, wall collapses occur due to the fact that the rock has an unstable structure. Signs of collapse are increased pressure, higher viscosity of the fluid that is used for flushing, and an increased number of rock pieces that come to the surface.

Fluid absorption most often occurs if the underlying formation completely takes the solution into itself. Its porous system or high absorbency contributes to this phenomenon.

In the process of drilling a well, a projectile that moves clockwise reaches the bottom hole and rises back. The drilling of the well reaches the bedrock formations, into which a tie-in takes place up to 1.5 meters. To prevent the well from being washed out, a pipe is immersed at the beginning, it also serves as a means of carrying the flushing solution directly into the gutter.

The drill string as well as the spindle can rotate with different speed and frequency; this indicator depends on what types of rocks need to be punched, what diameter of the crown will be formed. The speed is controlled by a regulator that regulates the level of load on the bit used for drilling. In the process of work, the necessary pressure is created, which is exerted on the walls of the face and the cutters of the projectile itself.

Well drilling design

Before starting the process of creating an oil well, a project is drawn up in the form of a drawing, which indicates the following aspects:

- Properties of the discovered rocks (resistance to destruction, hardness, degree of water content).

- The depth of the well, the angle of its inclination.

- The diameter of the shaft at the end: this is important for determining the extent to which the hardness of the rocks influences it.

- Well drilling method.

The design of an oil well must begin with determining the depth, the final diameter of the mine itself, as well as the level of drilling and design features. Geological analysis allows you to resolve these issues, regardless of the type of well.

Drilling methods

The process of creating a well for oil production can be carried out in several ways:

- Shock-rope method.

- Work with the use of rotary mechanisms.

- Drilling a well using a downhole motor.

- Turbine drilling.

- Drilling a well using a screw motor.

- Drilling a well with an electric drill.

The first method is one of the most well-known and proven methods, and in this case the shaft is pierced by chisel strikes, which are produced at regular intervals. Impacts are made through the influence of the weight of the chisel and the weighted rod. The lifting of the equipment is due to the balancer of the drilling equipment.

Work with rotary equipment is based on the rotation of the mechanism with the help of a rotor, which is placed on the wellhead through the drilling pipes, which act as a shaft. Drilling of small wells is carried out by participating in the process of the spindle motor. The rotary drive is connected to a cardan and a winch: such a device allows you to control the speed at which the shafts rotate.

Turbine drilling is performed by transmitting torque to the string from the motor. The same method allows you to transfer the energy of hydraulics. With this method, only one channel of energy supply at the bottomhole level functions.

A turbodrill is a special mechanism that converts hydraulic energy in fluid pressure into mechanical energy, which provides rotation.

The process of drilling an oil well consists of lowering and raising the string into the mine, as well as holding it in the air. A column is a prefabricated structure made of pipes that are connected to each other by means of special locks. The main task is the transfer of various types of energy to the bit. Thus, a movement is carried out, leading to the deepening and development of the well.

Drilling market is a key driving force behind the Russian oilfield services market. Drilling accounts for more than 30% of the total oilfield services market (in monetary terms). Together with drilling services (including support horizontal drilling) and other services that are used in the construction of wells, this share exceeds 50%.

During 2016, new trends emerged in the drilling market, which significantly affect the prospects for market development and are of fundamental importance for the adoption strategic decisions market participants.

. In 2016, Russia achieved historical maximum oil production in the amount of 547.5 million tons. Active growth in oil production was primarily due to an increase in meterage in drilling - by 23.2% in 2015-2016. The growth in production over the same two years amounted to 3.8%.

In accordance with the agreement on limiting oil production dated December 10, 2016, Russia undertook to reduce production from the level of October 2016 by 300 thousand barrels per day, or by 2.7%. Expected that production in 2017 will decrease by about 0.5% compared to 2016, and in the subsequent period, production will show moderate growth and reach the level of 570 million tons in 2025.

In 2017, despite the limitation of oil production, the drilling market expects increase in drilling volumes by 8-10% from the level of 2016. This is due to the need to maintain production at old, depleting fields.

In the medium term, drilling will mainly focus on maintaining production levels. Starting from 2018, there will be trend associated with moderate growth of the drilling market in physical terms and outstripping growth in monetary terms.

The share of horizontal drilling in production will continue to increase: from 11% in 2010, it has grown up to 36% in 2016, and by 2021 it will reach 44-46%.

In exploration drilling, the decrease in volumes in 2015 was replaced by a 3% increase in 2016. In the period up to 2026, it is predicted comparable volumes of exploration drilling due to the growing importance of additional exploration in mature fields.

share open market in drilling continues to decrease: in 2016 it amounted to 44% with the prospect of further reduction due to market consolidation by Rosneft.

As a consequence of key market trends, significant increase in competition between contractors, as well as increased price pressure on them from customer companies.

The analytical report aims to provide expert support for making strategic and operational decisions to a wide range of market participants, based on the following key elements of the study:

Grade key factors and development trends, including both common to oil and gas industry RF, and specific to the drilling market and its key segments.

Market size forecast for the period up to 2026 for production (separately horizontal) and exploration drilling. The forecast is formed in the context of the main regions of oil production and taking into account the peculiarities of drilling in each of them.

Analysis of customers and the competitive environment of contractors, including an assessment of the fleet of drilling rigs and the scope of work.

Report contains a basis for assessing the potential of the entire range of drilling-related service and equipment segments, including drilling services, horizontal drilling support, primary cementing, well completion, and others.

Around sources for the formation of the report were: RPI knowledge base, company data, industry statistics, assessments of industry experts.

"Russian Market of Oil Drilling" Designed for the following industry audience:

Oil and gas producing companies

Oilfield service companies

Manufacturers and suppliers of oil and gas equipment

Banks and investment companies

"Russian Market of Oil Drilling" is the first of a series of reports on the main segments of the Russian oilfield services market. The reports analyze the current state and development prospects until 2025 in the following segments:

1. Support for directional drilling(69,500 rubles)

2. Sidetracking (69,500 rubles)

3. Well workover (69,500 rubles)

4. Hydraulic fracturing (69,500 rubles)

5. Seismic exploration (69,500 rubles)

6. Coiled tubing(64,500 rubles)

1. Introduction

2 Main findings of the study

3 Oil and gas condensate production in Russia in 2006-2016 and production forecast for the period up to 2026

3.1 Production of oil and gas condensate in Russia in 2006-2016 by companies

3.2 Production of oil and gas condensate in Russia in 2006-2016 by regions of oil production

3.3 Forecast of annual oil production in Russia for the period 2016-2026

4 Volume of the Russian oilfield services market in monetary terms

4.1 Methodology for calculating the size of the oilfield services market

4.2 Size of the oilfield services market in 2005-2016

4.3 Forecast of the volume of the oilfield services market for 2017-2026

5 Current state drilling market

5.1 Dynamics of meterage in drilling in 2001-2016

5.2 Dynamics of production drilling in 2006-2016

5.3 Dynamics of exploration drilling in 2006-2016

5.4 Volume of the drilling market in monetary terms in 2006-2016

5.5 Main production trends in the drilling market

5.5.1 Development of horizontal drilling

5.5.2 Change in capital costs in production drilling

5.5.3 Effects of measures to increase production levels

5.6 Key Technology Trends in the Drilling Market

5.7 Current management challenges and trends in the drilling market

5.7.1 Well Construction Management Issues

5.7.2 Formation of the estimated cost of well construction

5.7.3 Development of time standards

5.7.4 Risk management of well construction projects

6 Forecast of the dynamics of drilling volumes for 2016-2026

6.1 Forecast methodology

6.2 Production drilling forecast for 2017-2026

6.3 Horizontal drilling forecast for 2017-2026

6.4 Forecast of exploration drilling volumes for 2017-2026

6.5 Forecast of drilling market volumes in monetary terms for 2017-2026

7 Major customers in the drilling market

8 Analysis of the competitive environment in the drilling contractor market

8.1 Drilling market in Russia by drilling contractors

8.2 Production capacity major drilling contractors

8.3 Activities of drilling contractors by region

8.4 Major M&A transactions in the drilling contractor market in 2016

9 Profiles of main contractors

9.1 Independent drilling contractors

9.1.1 Eurasia Drilling Company Ltd.

9.1.2 OOO Gazprom Burenie

9.1.3 ERIELL

9.1.4 Integra-Bureniye LLC

9.1.5 Catoil-Drilling LLC (Petro Welt Technologies Group of Companies, formerly C.A.T. oil AG)

9.1.6 KCA Deutag

9.1.7 Nabors Drilling

9.1.8 NSH ASIA DRILLING LLC (“Neftserviceholding”)

9.1.9 Group of companies (GC) "Investgeoservis"

9.1.10 CJSC Siberian Service Company (SSC)

9.1.11 TagraS-Holding LLC (MC Tatburneft LLC, Burenie LLC)

9.2 Drilling divisions of vertically integrated companies

9.2.1 Drilling subsidiaries OJSC Rosneft

9.2.2 Drilling unit of NGK Slavneft

9.2.3 Drilling subdivisions of Surgutneftegaz

Graph 3.1. Dynamics annual volumes oil and gas condensate production in Russia in 2006-2016 by companies, million tons

Graph 3.2. Distribution of increase in oil and gas condensate production in Russia in 2016 by producers, million tons

Graph 3.3. Share of manufacturing companies in oil and gas condensate production in Russia in 2016, %

Graph 3.4. Dynamics of annual volumes of oil and gas condensate production in Russia in 2006-2016 by regions of oil production, million tons

Chart 3.5. Distribution of growth in oil and gas condensate production in Russia in 2016 by regions of oil production, mmt

Graph 3.6. Forecast of dynamics of annual volumes of oil and gas condensate production in Russia in 2016-2025 by regions of oil production, million tons

Graph 3.7. Forecast of dynamics of annual volumes of oil and gas condensate production in Russia in 2016-2025 by types of deposits, million tons

Graph 4.1. Annual total volumes of the Russian oilfield services market in 2005-2016, billion rubles, % of annual growth

Graph 4.2. Specific shares of segments of the Russian oilfield services market in 2016, % of the total market volume in monetary terms

Graph 4.3. Contribution of segments to the total volume of the Russian oilfield services market in 2016, billion rubles

Graph 4.4. Forecast of Russian oilfield services market in 2017-2026, billion rubles, % annual growth

Graph 4.5. Forecast volumes of segments of the oilfield services market and their specific shares in 2026, billion rubles, %

Graph 4.6. Forecast shares of segments of the Russian oilfield services market in 2017-2026, % of the total market volume in monetary terms

Graph 4.7. Specific shares of segments of the Russian oilfield services market in 2017-2026, % of the total market volume in monetary terms

Graph 5.1. Production and exploration drilling in Russia in 2001-2016, mln. m 30

Chart 5.2. Completed wells in production and exploration drilling in Russia in 2006-2016, units

Graph 5.3. Average depth of one completed well in production and exploration drilling in Russia in 2006-2016, m

Graph 5.4. Influence of an increase in the number of wells and an increase in the depth of wells on the volume of penetration in production and exploration drilling in Russia in 2006-2016, %

Chart 5.5. Production drilling in Russia in 2006-2016 in the context of oil production regions, million m

Graph 5.6. Development drilling in Russia in 2016 in the context of oil production regions, million m

Graph 5.7. Commissioning of wells completed in production drilling in Russia in 2006-2016 by regions of oil production, units

Graph 5.8. Average depth of one completed well in production drilling in Russia in 2015-2016, m

Graph 5.9. Exploration drilling in Russia in 2006-2016 in the context of oil production regions, million m

Chart 5.10. Number of wells completed in exploratory drilling in Russia in 2006-2016 by regions of oil production, units

Chart 5.11. Average depth of one completed well in exploratory drilling in Russia in 2015-2016, m

Chart 5.12. Dynamics of the drilling market in monetary terms in 2006-2016, billion rubles

Graph 5.13. Dynamics of the volume of the drilling market in monetary terms in 2006-2016 by regions of oil production, billion rubles

Graph 5.14. Dynamics of the volume of horizontal and directional drilling in Russia in physical terms in 2006-2016, million m

Chart 5.15. Dynamics of the number of wells completed in horizontal and directional drilling in Russia in 2006-2016, units

Graph 5.16. Average depth of one completed well in production and exploration drilling in Russia in 2006-2016, m

Graph 5.17. Average depth of one horizontal well completed in Russia in 2016, m

Graph 5.18. Average depth of one directional well completed in Russia in 2016, m

Graph 5.19. Dynamics of changes in capital costs per 1 meter of production drilling in Russia in 2006-2016, thousand rubles per m

Chart 5.20. Dynamics of changes in capital costs per 1 m of production drilling for customers in Russia in 2015-2016, thousand rubles per m

Chart 5.21. Effects on the increase in oil production from the commissioning of new wells and geological and technical measures in Russia in 2006-2016, million tons

Chart 6.1. Dynamics of changes in monthly drilling footage in Russia in 2012-2017, million m

Graph 6.2. Forecast of annual meterage in production drilling in Russia for the period 2016-2026, million m

Chart 6.3. Forecast of annual meterage in production drilling in Russia at new fields for the period 2016-2026, mln. m

Chart 6.4. Forecast of the share of drilling at new fields in development drilling in Russia in 2017-2026, %

Chart 6.5. Forecast of annual meterage in horizontal drilling in Russia for the period 2016-2026, million m

Graph 6.6. Forecast of annual meterage in exploratory drilling in Russia for the period 2016-2026, million m

Graph 6.7. Forecast of the volume of the production drilling market by oil production regions in Russia for the period 2016-2026, billion rubles

Graph 6.8. Forecast of the volume of the horizontal drilling market by regions of oil production in Russia for the period 2016-2026, billion rubles

Graph 6.9. Forecast of the volume of the exploratory drilling market by oil production regions in Russia for the period 2016-2026, billion rubles

Drilling volumes in Russia have fully recovered after the crisis of 2014–2015, when lower oil prices and sanctions led to a reduction in investment in the domestic oil industry. At the same time, drilling is becoming more technologically complex and expensive, but experts believe that the current peak in drilling volumes will not last long. On trends in the Russian drilling services market in the review of "Siberian Oil" The article uses materials from a study of the service market in the oil industry, provided by the Tekart company. .

Ups and downs

After the crisis of 2009 in 2010-2013. in Russia, there was a dynamic increase in the volume of penetration in drilling. During this period, production directional drilling was most actively used. The increase in footage in production drilling over this period amounted to 26.1%, and in exploration drilling - 14.9%.

In 2014, the situation changed: oil prices fell, Russia found itself under sanctions from the EU and the USA, as a result of which investment activity decreased, and drilling volumes again decreased. However, this figure was also affected by another factor: the growth of horizontal drilling, which makes it possible to obtain a higher well flow rate compared to directional drilling. The scope of work in this area from 2008 to 2015. increased by 4.3 times. According to Techart, the share of horizontal drilling in total production drilling in 2016 amounted to 33.5% (8.3 million m).

As a result, the drop in total penetration in 2014 was 4.1% compared to 2013. At the same time, exploratory drilling, on the contrary, increased by 21.6%. A year later, the picture changed to the opposite: development drilling won back the fall of 2014, while exploration drilling, on the contrary, decreased. 2016 was characterized by an increase in both development and exploration drilling. According to the results of 2016, the meterage in production drilling amounted to 24.8 million meters (+14.5%), in exploration drilling - 910.0 thousand meters (+6.1%).

In monetary terms, however, the changes in the market looked different. Due to the complication of production conditions, the depletion of traditional fields, in recent years, the demand for such technological services as sidetracking and horizontal drilling has been growing, the average well depth and, accordingly, the amount of investment per meter of penetration has increased.

The structure of the Russian service market in the oil and gas industry

by type of service in 2016, % of the total volume in value termsInfographic: Daria Gashek

The growth of work in new regions with more difficult conditions (when developing new fields in Eastern Siberia, the Timan-Pechora region, etc.) also necessitates higher costs. The lack of infrastructure in the regions and difficult natural conditions require the availability of specialized machinery and equipment, which leads to higher prices and an increase in the average cost of a well.

According to the CDU of the Fuel and Energy Complex, in 2016 the total volume of investments in production and exploration drilling for all companies producing oil in Russia amounted to 673.5 billion rubles. (11.1 billion dollars). The increase in investment in production drilling compared to 2015 is estimated at 19.4%. Investment in exploratory drilling increased to 9%.

Share of horizontal drilling in Russia

in 2011–2016,

% of total production drilling

Compound Annual Growth Rate (CAGR) of investment in drilling in 2011–2016 amounted to 13.4%. At the same time, due to changes in exchange rates, the average indicator for the same period in dollar terms showed a negative trend (-1.9%).

In 2016 average cost penetration of one meter in production drilling, calculated as the ratio of the volume of investments to the total indicator of penetration, increased by 4.2% (in ruble terms). The same trend was observed in exploration drilling. The average cost of penetration showed continuous growth during 2011-2016. and in 2016 it reached the level of 57.9 thousand rubles/m for production drilling and 25 thousand rubles/m for exploration drilling.

Major Players

All oilfield service companies currently represented on the Russian market are conventionally divided by analysts into three groups.

The first includes service divisions within VIOCs: NK Rosneft, service divisions of Surgutneftegaz, Bashneft, Slavneft, etc. It should be noted that if in 2009–2013 service divisions were actively withdrawn from VIOCs, the current trend, on the contrary, was the development by oil and gas companies of their own or affiliated service.

Dynamics of drilling volumes in the Russian Federation

in 2011–2016, %

Source: Tekart based on data from the CDU TEK

Source: Tekart based on data from the CDU TEK

The second group is foreign service companies: Schlumberger, Weatherford (in August 2014, Russian and Venezuelan oilfield services assets were bought by Rosneft), Baker Hughes, as well as a number of second-tier companies (KCA Deutag, Nabors Drilling, Eriell and others).

The third group consists of large independent Russian companies with a turnover of more than $100 million. They arose as a result of the acquisition of oilfield services divisions of oil producing companies or as a result of the merger of smaller service companies. These include BC Eurasia, Siberian Service Company, Gazprom Drilling (sold in 2011 to the structures of A. Rotenberg).

Average cost of penetration in drilling

in 2011–2016, thousand rubles

Source: Tekart based on data from the CDU TEK

Source: Tekart based on data from the CDU TEK

Currently, the leadership in the Russian drilling market in the oil and gas industry remains with large independent companies and structural divisions VINK. At the end of 2016, the TOP-3 market participants in terms of meterage in drilling (in descending order) included EDC (BK Eurasia and SGK-Burenie, previously owned by the Schlumberger group), service units of OAO NK Surgutneftegaz and "RN-drilling". In total, these three companies accounted for about 49% of drilling.

Experts assess the technological level of independent Russian service companies as “average”. So far, compared to the generally recognized leaders of the world market, they can offer standard services optimal price/quality ratio.

Service structures of VIOCs, in terms of technological possibilities are also at the middle level. As a rule, they have the closest ties with scientific branch institutes and have a number of unique patents. Their additional advantage is a large margin of safety and access to the funds of the parent company to finance the purchase of expensive fixed assets.

Foreign service companies, leaders in the global service industry, were the main technology suppliers in the Russian Federation in the early 2000s. Currently, players such as Schlumberger and Halliburton account for about 14% Russian market services in the oil and gas industry in monetary terms. However, they are not represented among the largest participants in the drilling services market.

Main competitive advantage large foreign companies - Newest technologies service. Foreign companies were among the first in Russia to start performing complex hydraulic fracturing operations, taking cementing services, drilling fluid preparation and other drilling support services to a new level, using coiled tubing technology for the first time, and offering modern software products.

Their main disadvantage is the high cost of services. It is for this reason that there is currently a decrease in the activity of foreign market participants in Russia. Practice shows that for simple drilling, Russian oil companies prefer to turn to domestic contractors. They use the services of foreign companies mainly in the implementation of complex projects - technologies and competencies in the field of integrated project management are in demand here.

It should be noted that for the world leaders in oilfield services in 2015–2016. after the record results of 2014, they were also unsuccessful on the scale of the global market. Annual turnover Schlumberger, Halliburton, Baker Hughes and Weatherford shrank by 50-60% to 2010 levels.

Drilling in trend

Russian drilling companies are not public and do not publish information about their fleets, so it is rather difficult to estimate their capacity. The Russian fleet of drilling rigs (DR) of all classes of carrying capacity, according to various estimates, is in the range from 1000 to 1900 units. At the same time, the fleet of operating equipment in 2016 amounted to about 900 drilling rigs, Techart analysts believe.

In terms of the equipment used, each of the groups of companies has its own characteristics of consumption of drilling rigs. Service departments of VIOCs, relying on the authority of the parent company and, as a rule, relatively high volumes of investment programs, often independently dictate the requirements for purchased units. For them, manufacturers are developing new modifications. Foreign contractors prefer to work with European and American equipment suppliers. Independent companies give priority to one or another supplier based on specific needs, ease of purchase and operation of equipment.

Alexey Cherepanov,

Head of Operational Efficiency Programs for Gazprom Neft’s Own Oilfield Services:

Given the introduction of new technologies for the use of big data, which penetrate almost all areas human activity, drilling efficiency will increase, due to which the profitability threshold of many fields will significantly decrease. With increasing drilling efficiency, as happened in the US during the shale revolution, the relationship between penetration and the number of drilling rigs will change or even disappear in an explicit form. In Russia, the process of transition to high-tech drilling has already begun, therefore, in the absence of general economic shocks, we should expect at least a quantitative change in functional relationships and trends in the next few years.

If in the early 2000s, drilling rigs of foreign production were practically not supplied to Russia, then starting from 2006, imported products gradually gained a foothold in the Russian market. First of all, priority was given to European and American plants (Bentec, Drillmec, National Oil Well Varco, etc.).

However, the demand for drilling equipment in 2006–2008 was active around the world, which led to a significant level of utilization of all major global manufacturers, which were taken advantage of by Chinese companies with a significant amount of idle capacity.

As a result, already in 2008, the share of Chinese drilling rigs, according to Techart, accounted for more than 60% of the Russian market in physical terms.

In 2011 and 2012 fundamental changes have taken place in the market: the share of imports has decreased. This was due to both the restoration of production at the Uralmash plant and the introduction of an import duty from 2012: 10%, but not less than 2.5 euros / kg. As a result, prices for Chinese drilling rigs soared by 30-40%.

Over the past four years, a rather stable ratio of domestic and foreign (primarily Chinese) products has been observed in the structure of purchases. In the first place is Russian technology(from 46% to 61%). It is followed by equipment imported from China (up to 39%). For 2015–2016 4 American-made units were imported to Russia.

At the moment, the main Russian players capable of producing demanded rigs with a payload capacity of 225–320 tons can manufacture up to 76 rigs per year, with 40 of them accounted for by the Uralmash plant.

Forecast for the future

The prospects for the drilling and related services market are largely related to the development of the service market in the oil and gas industry as a whole.

Despite the decline in oil prices, the drilling market is still attractive to investors. This is due to the need to maintain the current level of production and development of new fields.

Contrary to previous years' expectations, drilling peaked in 2016, according to Techart. In 2017, according to preliminary estimates, there will be a slight increase in the increase in penetration, since the implementation of projects in the Bolshekhetskaya depression (YaNAO) and the Yurubcheno-Tokhomskaya zone (Eastern Siberia) is scheduled for this year. In the near future, major projects for the development of fields with large volumes of drilling are not planned, therefore, in 2018-2020. the penetration rate is expected to fall to the level of 2016.

In addition to a slight increase in meterage in drilling, outpacing market growth in value terms is expected. This is due to the fact that maintaining production at existing fields involves significant difficulties, and oil companies are moving to the development of new fields in regions such as Eastern Siberia and the Timan-Pechora region, where higher costs are needed.

Many of the issues related to technical problems in exploratory drilling have been discussed earlier. In this issue, I would like to highlight a little the differences between drilling exploration and production wells.

Conventionally, the process of CONSTRUCTION of a well (according to all classifications, such an activity as drilling refers to construction) is divided into the following stages: preparatory work, rigging, drilling and fastening, testing. These stages are distinguished during the construction of both exploratory and production wells. But what is their difference, let's take a closer look.

Preparatory work - this is the construction of the foundation on which the drilling rig will be installed, the laying of access roads. As a rule, exploration wells are drilled single. The task of an exploratory well is to "feel" the insides within a specific area. When a decision is made to drill production wells in the field, it is already known what can be expected and drilling of one well is not limited. But it is very expensive to build a platform for each well and drill a well without deviating from the place of drilling. Therefore, during production drilling, they proceed as follows: several wells are drilled from one site and the so-called directional drilling is used. With such drilling, the wellbore deviates significantly from the place where drilling began, and such a deviation can reach from hundreds of meters to several kilometers. Since several wells need to be placed on one base, accordingly, the site should be bigger size. In addition, if wells are drilled from one site, then it would be nice not to dismantle the drilling rig after drilling the next well, but to drag it to drill the next well. Currently, such movement is carried out along specially laid rails.

In fact, when drilling exploration and production wells, Various types drilling rigs. Largely because of this, the second stage of well construction differs - rigging works. At this stage, the drilling rig is transported, it is installed, the operation is checked, and the necessary communications (pipelines, power lines) are carried out. The necessary additional equipment, diesel stations, a residential town, in which drillers will later live, are also transported and installed.

Often, when production drilling begins at a site, this site is already equipped: all communications have been laid, roads have been laid. Scouts, on the other hand, have to get to the place of work by helicopters and along winter roads that melt in the summer. Under such conditions, there is no question of any power lines. Basically, all drilling rigs designed for exploration drilling are powered by diesel drive units, which is different from production drilling rigs, which are more focused on electric drive. Although there are exceptions when production drilling is carried out at the site, but electricity has not been supplied there. In this case, powerful diesel power plants, generating electricity, from which drilling rigs operate.

In Western Siberia, at present, the most common drilling rigs for production drilling are BU-3000 EUK drilling rigs manufactured by the Yekaterinburg enterprise Uralmash.

Process drilling production wells is also different from drilling "exploration". The most important difference is that almost all production wells are directional, while exploration wells are vertical.

There are also horizontal wells. They also apply to production wells. In horizontal wells, the last string enters the reservoir at an angle and then runs horizontally through the reservoir. This allows you to achieve a larger area of contact between the casing and the reservoir.

At the stage of well testing, the casing pipe breaks through in the area of contact with the productive formation. For horizontal wells, the flow rate is much higher than that of conventional wells.

The deviation in the drilling process is achieved by including in the layout of the drilling part (between the drill pipe and the turbodrill) the so-called curved sub.

It simply connects the drill pipe and turbodrill, but the ends of the sub are at a slight angle (1-2 degrees) relative to each other, which allows you to give the hole a deviation during the drilling process. In this process, the role of the technologist is very large, which must correctly orient the layout during assembly and descent. However, no matter how great a technologist is, no one is limited to trusting his skills. When drilling directional wells (and especially horizontal ones), special navigation systems are used that allow you to track the location of the bit. The bottom hole assembly includes a special device that measures the necessary parameters and transmits them to the top, where they are recorded and interpreted. An interesting way to transfer them up - through the drilling fluid. The device located at the bottom produces shocks that are transmitted through the entire column of drilling mud upward.

Trial production well is also different from testing an exploration well. More often, even in production wells, this stage is called development. As a rule, several productive objects are tested near exploration wells, starting from the lowest one. Then the tested object is isolated by installing a so-called cement bridge and the next object is tested.

The most important operation during testing is perforation - punching the casing pipe in the interval of contact with the productive formation. To carry out this operation, a perforator is lowered into the well, in which special charges are laid. The perforator is installed at the level of the productive formation in the well and a signal is applied to it, which generates an explosion of directed charges. The charges penetrate the casing string, the cement behind it, and create additional cracks in the oil-bearing rock. The better the perforating charges, the more penetrating fractures they create in the reservoir. But often in production wells, perforation is not limited to the so-called hydraulic fracturing (HF). The essence of this operation is the injection of liquid under high pressure into the well, which creates additional cracks in the reservoir. The depth of such cracks can reach several meters.

Another difference between exploratory and production drilling is the volume of field geophysical surveys carried out in wells. In exploratory wells, a large amount of all kinds of research is carried out, while in production wells they try to limit themselves to only the most necessary. The cost of field geophysical research in exploration can be ten times higher than the cost of geophysicists for a production well.

| |

The term "production drilling"

Production drilling - this stage is a continuation of the work on the well that was started during exploration drilling. Development drilling is preceded by the development of the area where it is planned to be carried out, which is associated with the development of exploration drilling. So, in the area where development drilling is planned, all the necessary communications have already been carried out, roads have been built to ensure the process. Sometimes it happens that electricity is not supplied to the site for a number of reasons. Then diesel power plants are used, from which drilling rigs can already work. Drilling of production wells differs from exploration drilling precisely in that all production wells are directional, while exploration wells are vertical. For drilling directional or horizontal wells, special navigation systems are used that track the location of the bit. It is installed in the bottom hole assembly and measures parameters by transmitting them to the top using the drilling fluid. Production wells may also include horizontal wells. Their last column can enter the exploited formation at an angle and then take horizontal direction. Thus, a high degree of contact between the exploited formation and the casing is achieved. As a rule, horizontal wells have a higher flow rate than conventional wells.There is also another difference between production and exploration drilling. It consists in studies that are carried out directly in the wells. So, in exploratory wells, this volume of field geophysical research is very large, and in production wells it is limited only to the necessary minimum. Thus, the costs of studying an exploratory well are much higher than those of a production well.

Drilling rigs are used in production drilling. They may also differ from those used in exploratory drilling.

Since in the sixties there was a very high efficiency of exploratory drilling, and also many large deposits were discovered in the seventies, it was from that moment that all the main efforts were directed to drilling production wells. For an optimal balance between exploratory and production drilling, the experience of field development, as well as the development period, are taken into account.

The stage of production drilling ends with the process of testing the well, or in other words, its development. The main thing in testing a production well is the perforation process, which is an operation carried out in the well using firing devices to create holes in the casing that are the communication between the reservoir and the well.

Companies with production drilling in their news: TATNEFT , SLAVNEFT , RUSSNEFT ,