Financial assistance: application, amount, payment and taxation

Financial assistance refers to deductions of a non-productive nature. It does not apply to the performance of the enterprise. The provision of material assistance is provided for both employees in the company and those who have already left. Also, accruals can be made in favor of third parties for various reasons provided for in the legislation. Next, we will consider in more detail who is entitled to material assistance, what is the procedure for obtaining it.

Grounds for payments

The reasons for which financial assistance may be paid are:

- Vacation care.

- Compensation for damage caused by any emergency.

- Holidays.

- The death of a relative of an employee, and so on.

For one reason, deductions are made in favor of most or all employees. For example, this applies to vacation pay. It acts as a one-time financial aid. In other cases, the allowance is granted under special conditions. For example, a worker or other person can apply for financial assistance (a sample of it will be given below) when it becomes necessary to purchase medicines, bury a relative, or meet other needs. Such deductions are of a social nature.

Value

The amount of financial assistance is set by the head of the company. The value can be determined in absolute terms or be represented by an amount that is a multiple of the official salary, taking into account the specific case and the financial capabilities of the enterprise. The procedure in accordance with which the deduction is carried out may be provided for in a labor or collective agreement. The income received from the current activities of the company acts as a source for the payment of material assistance. The decision on the need to distribute cash benefits at the enterprise is made by its head.

Taxation of material assistance

Due to the variety of reasons why this type of payment can be made, business accountants often have questions about how these amounts are reflected in the accounting. Financial assistance is shown in the reporting, depending on whether it is established in the employment contract or not. So, it will be recognized as a non-operating expense and taken into account on the account. 91.2 "Other expenses", unless specified in the agreement. If material assistance is prescribed in the contract, then it is the cost of salary.

Benefits for former employees

According to PBU 10/99 (paragraphs 4 and 12), such deductions are included in non-operating expenses. Therefore, they are reflected on account 91 - "Other expenses and incomes", sub-account "Other expenses". Since these costs are not taken into account when taxing profits, due to the appearance of a constant difference in the accounting of an enterprise, a tax (permanent) liability should be reflected. It is fixed by Dt sc. 99 "Profit and Loss" in correspondence with Kt sc. 68, which shows the calculations for mandatory contributions to the budget. Financial assistance to an employee is not considered a remuneration for his work and does not apply to compensation and incentive payments. Therefore, it is not subject to percentage allowances and regional coefficients, which are established for persons carrying out their professional activities at enterprises located in the regions of the Far North and equated to them.

Holds

In practice, situations often arise when material assistance to an employee is due in accordance with some reason, but alimony should be collected from his income. The types of those receipts from which such deduction is carried out are established in the corresponding list. So, for example, if a citizen receives material assistance in connection with a natural disaster, theft of property, fire, death, injury from him or his relatives, alimony is not collected from her. There is no deduction from the allowance due at the conclusion of marriage. Alimony is not deducted if material assistance is assigned at the birth of a child.

Documenting

Since there is no unified form, some difficulties arise. In accordance with Art. 9, paragraph 2, Federal Law governing accounting, documents for which special forms are not provided can be accepted if the necessary details are available. Therefore, material assistance to an employee can be accrued upon receipt of the appropriate order, which contains:

- Name of the act.

- Date of preparation.

- Company name.

- Contents of operation.

- Indicators in monetary and physical terms.

- Positions of employees responsible for the transaction and the correctness of registration, as well as their personal signatures.

Grounds for non-inclusion in labor costs

Before giving legal arguments, the very concept of salary should be clarified. It is defined in Art. 129 TK. Remuneration is recognized as a system of relations that are associated with the establishment and implementation of payments to employees for their professional activities under the law, other regulations, collective or labor contracts, agreements, local documents. The salary depends on the qualification, quality, quantity and complexity of the activity. Financial assistance does not fall into this category, as it:

- It does not apply to the performance by the employee of his professional duties.

- Does not apply to the activities of the enterprise as a whole, aimed at acquiring benefits. This means that it does not reduce the tax base.

The Tax Code establishes that such assistance is formed without taking into account the costs of any types of remuneration, except for those specified in the employment contract. According to the code, the amounts of material assistance are not taken into account when calculating the tax base.

Contributions to the FIU

They are also not deducted from the accrued financial assistance. Since it has a social dimension and is not considered part of the salary, the exemption from the withholding of the contribution is consistent with the principles according to which pension insurance is carried out. In particular, the labor pension should be formed primarily at the expense of amounts, the amount of which is established taking into account the qualifications of the employee, the quality, complexity and conditions of his professional activity.

Contributions to the FSS

These fees are not payable on payments such as:

- Financial assistance at the birth of a child during the first year of his life (no more than 50 thousand for each).

- Allowance for a citizen who suffered in a terrorist attack on the territory of Russia.

- Financial assistance to an employee in the event of the death of his relative.

- An allowance due to a natural disaster or other emergency that caused a citizen material damage or harm to health.

From this we can conclude that the insurance premium should be withheld from the amounts provided to individuals on other grounds. FSS employees believe that deductions from material assistance should be carried out. However, there is another point of view on this matter. It is based on the following arguments:

- The basis for calculating the insurance premium is wages (income).

- Financial assistance does not apply to such income, since it is not provided for when calculating salary. When granting benefits, the results of specific activities of employees are not taken into account.

- Expenses for the payment of material assistance are not taken into account when establishing the tax base. This is due to the fact that they are not produced from the wage fund, but from net income.

It follows from this that in each specific situation, the management of the enterprise will have to independently decide whether it is necessary to withhold insurance premiums from benefits or not in cases that are not provided for by law. When a positive decision is made, it is likely that the boss will have to defend his order in court.

personal income tax

In Art. 217 of the Tax Code establishes a list of income received by employees that is not subject to taxation. These, in particular, in addition to the above payments, include amounts not exceeding four thousand rubles a year.

This, for example, can be vacation pay, financial assistance in difficult financial situations, retired former employees, and so on. Personal income tax will be withheld from amounts exceeding 4 thousand rubles a year.

Bid

Material assistance is recognized as income subject to taxation at the rate of 13%, if the non-taxable limit is exceeded. Standard deductions are provided by the organization that acts as a source of income, at the choice of the payer in accordance with his written request and documents that confirm the right to these deductions. If cash assistance is given to former employees who are retirees, they may receive these deductions provided that they apply before the end of the year. If the benefit is deducted to the worker's account every month during the calendar year, the deductions are made from the beginning of the relevant period. At the same time, the total amount of material assistance is reduced by 4,000 rubles (non-taxable amount). In personal income tax accounting, which is withheld from an amount exceeding 4 thousand rubles, should be reflected in the following entry: Dt 70 (76) Kt 68, subaccount. "Calculations on personal income tax".

Poor and vulnerable categories

Persons included in these categories are provided with one-time material assistance. It can be provided either in cash or in kind. A one-time allowance is paid from the local, federal and regional budgets, extra-budgetary funds under programs approved by authorized state authorities annually. Such amounts are also exempt from personal income tax.

Providing reporting

Tax agents - enterprises acting as a source of payment of income listed in Art. 217, paragraph 8, are required to keep records of the amounts provided, regardless of their size. Information about these charges is provided to the appropriate authority in the form No. 2-NDFL. In the course of filling out the reporting, enterprises indicate the full amount of these incomes for each basis for the period and a tax deduction not exceeding 4 thousand rubles. If assistance is accrued to a former employee in the amount of less than 4 thousand rubles, the enterprise must provide information about this to the tax authority in the form No. 2 of personal income tax.

Profit deductions

According to Art. 270, paragraphs 23 and 21 of the Tax Code, material assistance to employees of the enterprise, regardless of its grounds, is not included and is not taken into account when taxing profits. This provision applies regardless of whether the benefit is provided for in the employment or collective agreement or not. In order to avoid discrepancies between tax and accounting records, it is inappropriate to include material assistance in the documentation regulating the system of remuneration for the labor activity of employees. Expenses that relate to the provision of benefits to former employees of the organization also do not reduce the amount of accounting profit. This is due to the fact that, according to paragraph 16 of Art. 270 of the Tax Code, when determining the tax base, expenses in the form of the value of property transferred free of charge are not taken into account. This category includes works, services, rights in rem, as well as securities and cash.

Package of documents

An employee who needs additional funds must write an application for financial assistance. The following documents must be attached to this paper:

- At the death of a family member - a copy of the death certificate, if necessary - copies of acts confirming kinship (birth certificate, marriage certificate).

- Decisions of state authorities, certificates from the SES, DEZ and other authorities confirming the fact of an emergency.

- Papers certifying the occurrence of a terrorist attack on the territory of Russia (for example, a certificate from the Ministry of Internal Affairs).

- Birth certificate of the child if necessary to receive money for his maintenance.

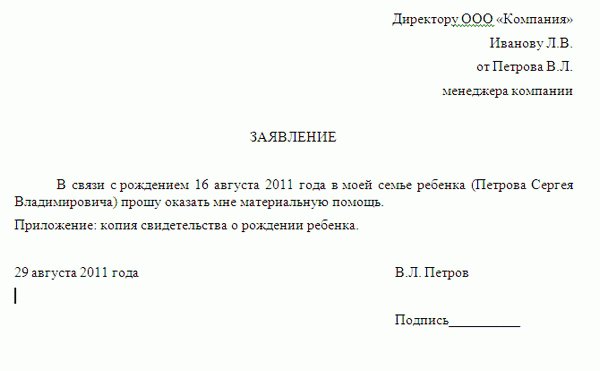

Application for financial assistance: sample

The document should contain information about who the request is addressed to and from whom it comes. At the top right, the full name is indicated. head of the enterprise, position, name of the company, as well as full name. and position of the employee. Below in the center should be written the word "statement". Further, a request is made for the provision of financial assistance, the reasons for this are indicated. As evidence of the reasons, the appendix provides a list of documents confirming the circumstances that were indicated in the content. Copies of papers must be attached to the application. At the very bottom, the signature and date of compilation are put. In the text, the applicant can also indicate the amount for which he expects.

Additionally

It should be noted that the cash benefit is not the duty of the manager, and the fact of writing an application, indicating the amount of expected assistance, as well as the circumstances that served as the reason for the appeal, do not give rise to the obligation of the manager to satisfy the request. The amount of the benefit indicated in the application can only serve as a guide for the employer. The final amount is set by the head, based on the financial situation at the enterprise and the complexity of the circumstances of the applicant. If the manager decides to grant the request, an appropriate order is drawn up. Based on it, the applicant will receive a sum of money at the cash desk of the enterprise.

Finally

The NC does not clearly define who should be recognized as members of an employee's family. In accordance with Art. 2 of the Family Code, they include children, parents (adopted, adoptive parents), spouses. In this case, the fact of cohabitation does not matter. Paragraph 1 of Article 11 of the Tax Code provides that the terms, concepts and institutions of family, civil and other branches of law are used in the meaning in which they are directly applied in them, unless otherwise provided by law. This, in turn, means that material assistance paid to members of the employee's family is also exempt from personal income tax. Appropriate evidence must be provided to support this right.