Dismissal of the chief accountant at his own request

Often its importance for the enterprise is so great that the figure of the chief accountant is rightfully placed on a par with the head. It is not surprising that the decision to dismiss the chief accountant of his own free will will not leave the team and its head indifferent. At the same time, the Labor Code of the Russian Federation does not single out the chief accountant from the general mass of other employees and does not contain special articles on the topic of his dismissal on his own initiative. So, having written a statement, the chief accountant will leave the workplace after 14 days, and no one can legally prevent him from doing this (Article 80 of the Labor Code of the Russian Federation).

Not a single article of the Labor Code of the Russian Federation contains additional conditions or features for the dismissal of the chief accountant of an enterprise on a personal initiative. The warning period and procedures do not depend on the organizational and legal form of the enterprise or its form of ownership.

Procedure for the transfer of cases

The written application starts the difficult and thorny path of transferring cases from the departing employee to the new one. Since the law does not contain clear requirements regarding the mandatory nature and form of the act of acceptance and transfer of cases, it is possible to approve it and specify the details of the process in the order of the head (Article 8 of the Labor Code of the Russian Federation):

- Full name and positions of participants in the transfer (a new chief accountant, deputy, any other employee or the head of the enterprise himself can be appointed as a successor).

- The timing and completion of the procedure.

- Date of separation of responsibility (the last period is determined, which must be completely closed by the old chief accountant, including the last reporting period and its list).

- Range of issues for verification (balance sheet, account balances, statements of synthetic and analytical accounting, breakdown of receivables and payables, etc.)

- The list of property, documents and other valuables subject to safekeeping with the new head of accounting (originals of title documents, information carriers on electronic signatures, seals and stamps, keys to safes and their contents).

- Data of officials entitled to be present during the transfer.

- Form of the final document.

Even if the new chief accountant has already been found and is ready to start working, this will not be enough to sign the act of acceptance and transfer of documents. The fact is that the signature in such a document means the acceptance of all papers and valuables for storage and use, and only an employee of the enterprise can do this. This means that on the date of signing the act, an employment contract must be drawn up with a person. Since two chief accountants in one enterprise is nonsense, it is better to accept a candidate for the position of chief accountant as his deputy or one of his deputies. And then transfer him to an already vacant post.

If there is no desire to produce personnel orders, then the head himself can sign the act of transfer. Moreover, paragraph 1 of Art. 7 402-FZ directly obliges him to organize the safety of documentation in the company. It must be remembered that in this case, you will need to go through the transfer procedure again. Now the act will be signed between the head and the new chief accountant who has taken office. Otherwise, it will not work to make him responsible for documents and valuables.

What should be transferred?

It is interesting for all parties to document the process of transferring cases upon dismissal of the chief accountant of their own free will. Both the incoming and the outgoing specialist will be able to protect themselves from the boss and inspectors with a detailed list of documents and information listed in the act. Therefore, if the question arises about what should be included in the final document, you need to use a simple rule: there is an accounting entry - there must be a primary document. In other words, if at one time the chief accountant entered a figure in the accounting registers or used it for reporting, then he must present to the new employee who takes office the paper from which it was taken.

Those who have experience in working as an accountant or auditor are well aware of how much primary documentation and documentation compiled on its basis can accumulate in an enterprise even for a short period of work. Well, if a documentary audit has already passed at the enterprise relatively recently, then documents are subject to transfer only for the subsequent period after the audit. You can simply familiarize yourself with the act following the results of the audit to make sure that the predecessor has complied with all the instructions set forth in it and paid all penalties.

Main List

Regardless of the specifics of the enterprise, there is an invariable list of transferred documents and valuables that the chief accountant must transfer upon dismissal:

- cash documents and reports;

- bank statements;

- accounting registers and turnover sheets of accounting;

- incoming and outgoing documents for inventory items;

- acts of work performed and services received;

- inventory cards of accounting, depreciation and movement of fixed assets, inventory sheets and inventories of the last inventory;

- acts of write-off of valuables, completion or reconstruction of fixed assets;

- advance reports and supporting documents;

- documents on targeted or state financing, if such operations have taken place in the company;

- loan agreements and annexes thereto;

- statements of accrual and payment to employees;

- estimates, cost estimates and technological maps.

In the act of transfer, it is also necessary to fix the balances on the accounting accounts as of the date of separation of responsibility specified in the order:

- the balance of funds in cash and on the current accounts of the enterprise, and it is desirable to immediately conduct their sudden inventory;

- decipher receivables and payables in the context of counterparties (consumers of the company's products and suppliers of goods and services);

- balances or overspending on accountable amounts in the context of materially responsible persons;

When drawing up the act, it would be useful to enter information that the new chief accountant is familiar with the order on accounting policies, the job description of the chief accountant, the regulation on bonuses and incentives for employees, the collective agreement and the charter of the enterprise. Also, all items and intangible assets stored by the previous chief accountant are transferred under the signature.

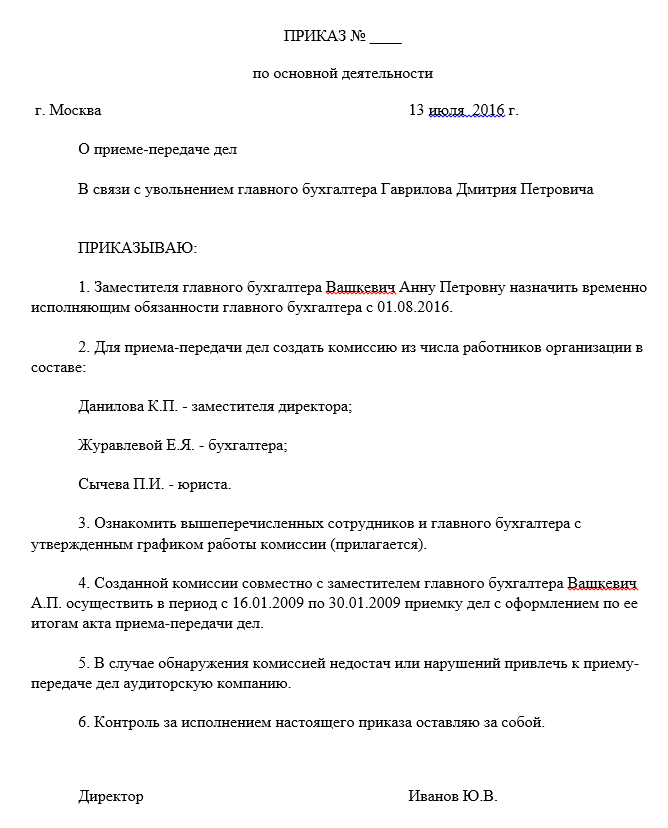

Sample order on acceptance and transfer of the case of the chief accountant:

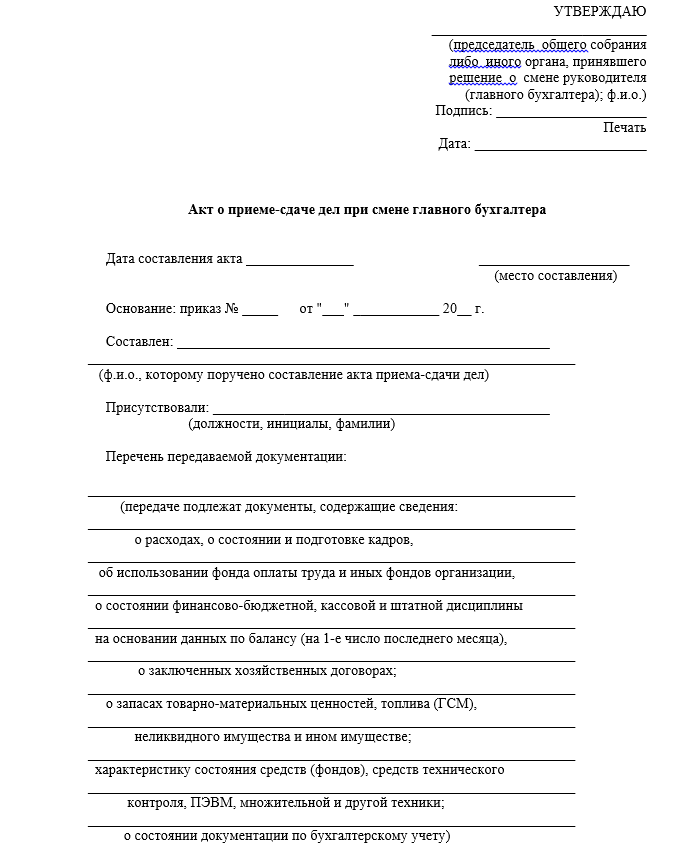

The act of acceptance and transfer of cases by the head office:

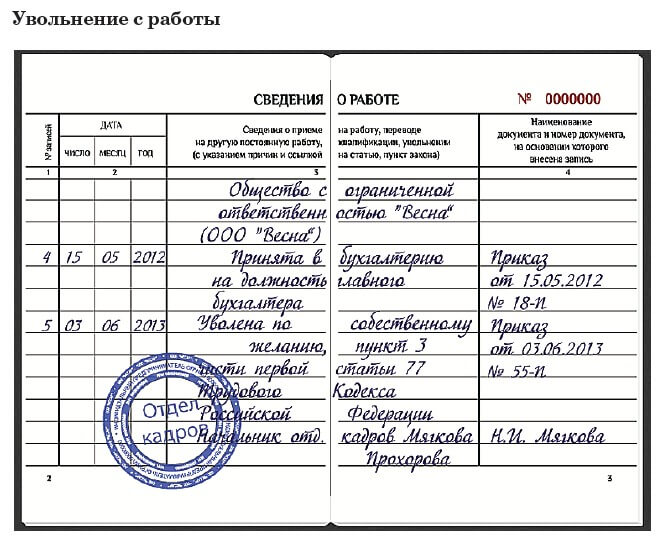

Sample entry in the work book:

Timing

If the company from which the chief accountant is leaving is quite young and the period of its activity does not exceed a couple of years, then you need to transfer documents for the entire period of work. If the life path of the company is much longer, then the parties to the transfer need to decide on the depth of verification and inventory of the archive:

| Date of last check | Document submission period | Base |

| Less than three years ago | The original audit report and all documents for the subsequent period are transferred | Art. 113 Tax Code of the Russian Federation |

| Three to five years ago | For the entire period from the date of the last check | Art. 23, paras. 8 p. 1 of the Tax Code of the Russian Federation |

| More than five years ago or never | For the last five full annual reporting periods | Art. 29 402-FZ |

| Regardless of the timing | Long-term storage documents (from 10 years), such as personal files of employees and payroll records, are handed over for the entire period of operation of the enterprise | Order of the Ministry of Culture of Russia No. 558 |

It is unlikely that the chief accountant has absolutely all the primary documents of the enterprise in storage, but it will be useful to know the terms of their storage for conducting an inventory in departments and areas in the accounting department. The new specialist needs to hand over only those papers that were personally maintained by the old chief accountant.

The obligation of the retiring chief accountant to transfer cases applies only to those documents that are under his direct control or provided to him under a safekeeping agreement.

What should I do if there is a shortage during the transfer?

One of the most important sections of the act of transfer of cases is the reflection of shortages and errors in documents. After all, it is often during the delivery of documents that the absence of primary documents or gaps in its completion is discovered. This may serve as a reason for the new accountant not to sign the act. It is clear that the correction or restoration is the responsibility of the former specialist, but he may not be able to do this before the date of dismissal or refuse to do it at all. Then you need to take out data on defects and violations in accounting, as well as the storage of documentation, in a separate section or find another way to notify management. The decision on who will fix the errors and how it will be paid is the responsibility of the authorities.

If the cases are not transferred according to the act, no matter who finds shortcomings in the maintenance of documentation or the safety of the primary, the responsibility will fall on the resigned chief accountant.

If there is no one to transfer cases to?

If the chief accountant's own desire was an unpleasant surprise for the employer, difficulties may arise with the search for a new specialist and the smooth transfer of cases. The boss will simply sabotage the process by not appointing a successor and not signing the act himself. And although his actions can be indirectly regarded as an attempt to detain a specialist, it will be problematic to prove this in the same court. Indeed, in the Labor Code there is not a word about how exactly this process should be organized, the enterprise is given complete freedom in this matter (Article 8 of the Labor Code of the Russian Federation).

You can partially protect yourself with the help of your subordinates, because the position of chief accountant, most often, implies the presence of several more accountants in the company. Each of them is responsible for his area of work, and, with the loyal attitude of these employees, you can try to sign with each of them your copy of the act on the integrity of documents for the current and previous periods.

If the enterprise is large enough, and there is an archival service in its structure, then it is most correct to hand over the papers to the archivist. In any case, it is better to spend the two-week warning period for the chief accountant on checking and putting all the cases in order, even if there is no one to hand them over.

Unlike a resigning manager, it will be difficult for the chief accountant to transfer the archive for storage to a third-party organization or take documents with him for independent storage.

Intentional harm and liability

Intentional sabotage in the form of destruction of any papers on the part of the management is unlikely, because the responsibility for the reliable reflection of accounting information and administrative responsibility for its violation extends to the director to the same extent. The norms of the Tax Code of the Russian Federation speak of the responsibility of the taxpayer (you need to understand - enterprises), and the Code of Administrative Offenses of the Russian Federation - of the responsibility of officials (that is, both the head and the chief accountant). So in this sense, the director and chief accountant are "in the same team" and the authorities will not harm the departed specialist in this way.

What will you be responsible for after leaving?

As in the case of the former head, the dismissal of the chief accountant will not be a reason to forget about everything and cross out the period of work in the company from life. At least for the next few years. Here is a non-exhaustive list of the most common reasons:

| Regulatory document | Article | Type of violation | statute of limitations |

| Tax Code of the Russian Federation | Art. 120 | Gross violations in accounting, including those that led to an underestimation of taxes (lack of primary documents or deliberate distortions in statements and reports) | 3 years from the end of the reporting period (Article 113 of the Tax Code of the Russian Federation) |

| Art. 122 | Late payment of taxes | ||

| Code of Administrative Offenses of the Russian Federation | Chapter 15 | Penalties due to violation of the deadlines for registration, reporting, misrepresentation in accounting, misuse of funds, etc. This article implies the personal responsibility of the officials of the enterprise. | 1 year from the date of discovery (Article 4.5 of the Code of Administrative Offenses of the Russian Federation) |

| Russian Criminal Code | Art. 198 | Tax Evasion | Minor violations - 24 months from the date of establishing the fact of the commission of a crime, medium gravity - 6 years, serious - 10 years (Article 78 of the Criminal Code of the Russian Federation) |

| Art. 165 | Damage caused by breach of trust | ||

| Art. 201 | Malpractice | ||

| Art. 293 | Negligent attitude towards work | ||

| Art. 327 | Forgery of documents | ||

| Labor Code of the Russian Federation | Art. 238 | Material damage due to the direct fault of the chief accountant (charged in the amount of average monthly earnings, if full material liability is not dissuaded in the employment contract, article 241 of the Labor Code of the Russian Federation) | 1 year from the date of clarification of the fact of damage (Article 392 of the Labor Code of the Russian Federation) |

Even if facts of violations or economic crimes were revealed at the enterprise after the departure of the chief accountant, he can be held liable only if there is intent or direct fault of the dismissed person.

Financial responsibility to the employer

The possibility provided for by Article 238 of the Labor Code of the Russian Federation to recover material damage from an employee provides only cases of direct, calculable financial damage. The favorite topic of some employers is about lost profits in the Labor Code of the Russian Federation is completely excluded.

Since Article 241 of the Labor Code of the Russian Federation limits the amount of liability to the size of the average salary, and the chief accountant is not included in the list of positions with which a separate agreement on full liability can be concluded, the obligation to compensate for damage can only be prescribed in an employment contract (Article 243 of the Labor Code). But even then, the employee retains the right to refuse to withhold material damage from the salary. In such circumstances, the employer will be forced to prove the need for compensation and the amount of damage in court (Article 248 of the Labor Code).

Audit as a way to reconcile the parties

It is unlikely that the chief accountant will suddenly decide to dismiss of his own free will. Behind a brief and streamlined wording, the thought of changing jobs, as well as the accumulated mutual dissatisfaction with the management, is often hidden for weeks or months. In this case, it may be acceptable for both parties to conduct an audit of the enterprise's activities over the past few years.

First, the auditors will do a full review of all documentation instead of a selective review, which is practiced in the standard transfer of cases between accountants. Secondly, if shortcomings are found, the company will be given recommendations on how to correct them or restore the missing papers. Thirdly, under an agreement with the auditing company, responsibility for all detected violations of tax or other legislation for the audited period will be assigned to the involved auditors.

Financial result of dismissal (compensation)

Since the Labor Code does not distinguish chief accountants from other employees, they also do not provide for special compensation payments upon dismissal of their own free will. On the day of dismissal, the chief accountant will receive a salary for an incomplete month worked, arrears in payments or accountable amounts, if any, and compensation for unused vacation days (Article 140 of the Labor Code).

Additional financial compensation can be prescribed in a collective agreement or an employment contract concluded with a specialist on an individual basis. The dismissal of the chief accountant is a significant event in the enterprise. Competent organization and consistent work on the transfer of cases will ensure the company's smooth work in the future, and the dismissed employee will only have good memories of the previous place of work.

Lawyer of the Board of Legal Protection. Specializes in handling cases related to labor disputes. Defense in court, preparation of claims and other regulatory documents to regulatory authorities.