Analysis of enterprise risks using an example. Fundamental research Assessment of economic risks using the example of an enterprise

1.3 Risk management

In the risk management system, an important role is played by the correct choice of measures to prevent and minimize risk, which largely determine its effectiveness. The risk reduction system includes certain methods and ways:

1. Obtaining comprehensive information about the upcoming choice and result.

2. Risk avoidance.

3. Diversification.

4. Reserving funds to cover unforeseen expenses.

5. Limitation.

6. Hedging.

7. Risk insurance, self-insurance.

8. Checking business partners and terms of the transaction. Business planning.

9. Recruitment of personnel for a business organization.

10. Transfer of risk.

11. Other methods.

The choice of a particular risk minimization method above depends on the experience and capabilities of the entrepreneur and any other manager. For a more effective result, a combination of methods is usually used.

In his activities, a manager encounters many risks, therefore, in addition to the basic methods of minimizing them, he uses specific methods that are used only in this case. Ways to minimize the most common risks are given in Table 1.2. (Appendix 2)

Indeed, actions aimed at mitigating risk can be very different. People enroll in extreme driving courses to reduce the likelihood of getting into an accident in difficult conditions - this is also a strategy for mitigating, minimizing, eliminating risk. The choice of one method or another depends on the specific situation, the degree of risk and the capabilities of the enterprise. This is what determines the fundamental decision: accept the risk, reducing its negative consequences using various methods, or avoid it.

In the process of carrying out business activities, a company may refuse to carry out financial transactions or activities associated with a high level of risk. This direction of risk neutralization is the simplest and most radical; it will completely avoid potential losses, but does not at all contribute to obtaining profits associated with risky activities.

When concluding any transaction, to reduce the risk of business contracts, the entrepreneur needs to check the prospective partner. The basic rule of business is “trust, but verify.” A possible way to avoid mistakes when choosing a partner is to create your own system for collecting and analyzing information about potential or existing counterparties. As an example in this case, you can use the Due Diligence system practiced by Western banks in relation to their clients. This system provides protection against various types of fraud. One of the main tools of such a system is a questionnaire, including questions about the name of the counterparty company and the addresses of its offices for the last two to three years; about the types of business it carries out. The questionnaire may contain questions about the company's partners and their addresses, it includes questions about the financial condition of the company and the expected turnover or future average account balance. The most difficult questions in the questionnaire are related to the origin of the company's capital. Such a questionnaire provides preliminary information about the client, and if something in his answers is alarming, additional research should be carried out, including a search for confirmation (or refutation) of the data received, a search for facts that the partner has kept silent about, as well as checking information through others counterparties.

Risk diversification is perhaps the most complex and interesting risk management method that requires high professionalism. It represents the use of the economic and mathematical concept of “negative correlation” in economic practice. Invested funds are directed to completely independent transactions and projects that are in no way related to each other. In this case, if a risk event occurs and losses occur on one transaction, you can count on a successful and profitable outcome of another. Moreover, it is advisable to focus on negatively correlated outcomes, that is, to choose investment values (objects) with directly opposite profitability vectors. Then profits on one transaction will be able to compensate for possible losses on another.

When forming a securities portfolio, the problem of risk diversification is given particularly serious attention. First of all, the “rule of a dozen” applies. It is necessary to ensure a sufficient variety of securities. Therefore, generally accepted practice dictates that a bank’s portfolio should contain at least twelve blocks of shares in a wide variety of companies. Next, pay attention to the level of profitability and degree of risk of the securities. High-yield securities typically involve a considerable degree of risk. Securities with acceptable risk yield correspondingly very moderate returns. And low-risk securities are ineffective and not interesting for the bank. The “five finger rule” offers a way out of this situation. It follows from it that to form an optimal portfolio, out of every five shares, one should be low-risk, three should be with normal, acceptable risk, and one should be high-risk, but also high-yielding.

In addition, the financial sector of the economy often uses a method of risk diversification, called “risk hedging.” Risk hedging involves limiting the amount of losses with financial instruments, but as a consequence, profits too. It is carried out in the form of concluding parallel financial compensation transactions, when a possible loss on one transaction is compensated by a possible profit on another. There are many ways to hedge risks, but the main, most used and frequently encountered are options, futures and swap transactions.

The next step in solving the problem of risk management is to study the possibility of full or partial self-insurance of the transaction. Self-insurance is nothing more than taking risks on oneself and, undoubtedly, is the cheapest (with the possible exception of renouncing risks) way of dealing with risks. It is assumed that possible damage will be covered with current funds or with the help of a reserve fund. Therefore, it is obvious that the use of self-insurance opportunities is very limited. Basically, this method is justified if the probability of a negative outcome and the amount of possible loss are not large.

When using self-insurance, you need to be aware that the cost-effectiveness of this method results in some negative aspects. First of all, this is the “death” of working capital. The company is forced to keep considerable funds in reserve; they cannot be counted on when concluding new, often interesting and effective contracts; it is impossible and dangerous to put them into circulation. However, there is still a danger that there will be a “streak of failures”: against the backdrop of low financial income, losses will occur one after another in a short period of time, and any reserve funds will still not be enough. All this causes uncertainty and nervousness among management, which will certainly be transmitted to the entire staff of the company. If loss prevention and self-insurance do not provide the desired protection against risk and only slightly reduce it, which is quite likely in modern business, one can apply the most common and widely used, already traditional method of risk management, which is insurance. The essence of this method is that the entrepreneur takes an insurance company as a partner in the transaction and assigns to it, after concluding the appropriate contract and paying insurance premiums, a significant part of the expected risks. Unlike all industries and spheres of the economy, where risk for an entrepreneur is an undesirable side effect, in the insurance business risks serve as the main field of activity. That is, the risks of the entrepreneur are assumed by the professional.

When deciding to use insurance, you need to keep in mind that, firstly, the risk must be random in nature, a negative outcome should not be pre-programmed and included in the transaction. Secondly, only losses that can be measured and assessed using natural and monetary indicators are insured. And finally, the risk itself cannot be the object of insurance. Such an object is the company’s inventory and cash assets [21, p.65].

Let us note that economic risks are an inevitable component of business activity, since they are immanent in the market. Risks cannot be eliminated, but it is quite possible to reduce possible losses. This can be achieved through the application of risk management techniques. Of course, risk management is associated with certain costs for the company, but its implementation is necessary and justified. By managing risk, a firm sacrifices less to save more. It replaces the possible occurrence of significant losses with relatively small, strictly defined costs of risk management.

Analysis of risks in the activities of an enterprise using the example of OJSC "Galantus"

In the risk management system, an important role belongs to the correct choice of measures to prevent and minimize risk, which largely determine its effectiveness...

Project Risk Analysis

Project risk management includes processes related to risk management planning, risk identification and analysis, risk response, monitoring and project risk management...

Comprehensive assessment of the risks of the financial and economic activities of an enterprise (using the example of PJSC TAIF-NK)

Financial risk management of a company is a specific area of financial management, which in recent years has become a special field of activity abroad - “risk management”...

Business risks and their management

Entrepreneurial risk

The main task of an entrepreneur is not to avoid risk altogether, but to make decisions related to risk management based on objective criteria. One of the main rules of entrepreneurial activity is: “Do not avoid risk...

Entrepreneurial risk

Any business organization inevitably faces various situations, unplanned or unforeseen events, to which it is necessary to respond adequately so as not to incur losses caused by these phenomena or...

Draft effective business plan for production and sales of products

Possible risks associated with the introduction of tulip forcing technology are: 1. Plant diseases 2. “Blind bud” - a physiological state of the plant in which it does not form a flower; 3. External factors (fires, floods, etc.)...

Industrial and financial group SCM (System Capital Management)

SCM Group has created an effective and reliable risk management system that combines the best global practices and its own developments in the business areas and markets where SCM operates...

Development of an investment project

Since the quality of the economic assessment of an investment project is determined by how complete and reliable information the decision maker has...

The essence of business risk

“The main task of an entrepreneur is not to avoid risk altogether, but to make decisions related to risk management based on objective criteria. One of the main rules of entrepreneurial activity is that you cannot avoid risk...

Economic risks of the company. Essence, types, methods of minimization

Identification and analysis of risks are only an integral part of risk management; risk prevention, its localization, division, compensation and other risk management methods contribute to changing the elasticity of the management system...

Send your good work in the knowledge base is simple. Use the form below

Students, graduate students, young scientists who use the knowledge base in their studies and work will be very grateful to you.

Posted on http://www.allbest.ru/

FEDERAL STATE BUDGET EDUCATIONAL INSTITUTION OF HIGHER PROFESSIONAL EDUCATION

"Tolyatti State University"

Institute of Finance, Economics and Management

Department of Accounting, Analysis and Audit

Course work

in the discipline: “Comprehensive economic analysis of economic activity”

on the topic: Analysis of risks in the activities of an enterprise using the example of JSC Galantus

Performed:

Tolkacheva N.

Group EKB-0901

Scientific adviser:

O.V. Schneider

Tolyatti-2012

Introduction

1. The essence of the occurrence of risks in the activities of the enterprise

1.1 The role and economic content of risks in the financial and economic activities of an enterprise

1.2. Classification and methods of risk assessment in enterprise activities

1.3 Risk management

2. Analysis of risks in the activities of the enterprise JSC Galantus

2.1 Technical and economic characteristics of JSC Galantus

2.2 Risk assessment in the activities of JSC Galantus

3. Ways to reduce and manage risks at JSC Galantus

Conclusion

List of used literature

Application

assessment of commercial risk economic activity

Introduction

The changes that have occurred in the Russian economy in recent years have revealed a number of controversial and topical problems that are theoretical and applied in nature and are extremely important for the sustainable functioning and development of the economy. Priority problems include issues of theory, methodology and practice of making management decisions under conditions of risk and uncertainty.

Risk is danger! Risk is a possible future qualitative or quantitative deterioration in the condition of an object. In economic literature, they usually start from these concepts. Threats of damage are characterized by the optionality of negative impact, uncertainty of parameters and consequences such as time, strength of manifestation, and amount of damage. These uncertainties are caused by ignorance of the law, lack of information and lack of skills in managing economic risks (insufficient qualifications of management personnel).

Any business involves risks. Any successful business is associated with great risks, and the success of the enterprise depends on how businessmen, managers, and executives cope with these risks. Some people manage risks intuitively, others consciously, but any activity requires analysis and further risk management for the successful and full development of the enterprise. The most important feature of entrepreneurship is the presence of risk both at the stage of creating an organization and during its further functioning. Any enterprise is at risk of losing property, valuables, money, that is, any type of economic resources, including labor and time, because labor losses and wasted time cause serious damage to the results of business activities. The main objectives of the risk management system can be formulated: increasing financial stability, improving risk management mechanisms. The purpose of this course work is to analyze the adoption of optimal management decisions taking into account the factor of uncertainty and risk using the example of a specific organization, JSC Galantus.

This goal determined the main objectives of the study, which were as follows:

· consider the concepts of uncertainty and risk;

· consider the process of influence of uncertainty and risk on the organization’s activities;

· consider scientific methods of decision-making recommended under conditions of uncertainty and risk;

· apply in practice the development of management decisions in conditions of uncertainty and risk using the example of the organization OJSC Galantus.

The object of the study is the uncertainties and risks relating to the activities of organizations in any industry, and the subject of the study is the adoption of management decisions aimed at obtaining the least losses in conditions of uncertainty and risk.

1. The essence of the occurrence of risks in the activities of the enterprise

1.1 The role and economic content of risks in financial and economiceconomic activity of the enterprise

As is known, a condition for the effectiveness of any market activity is considered to be economic freedom, which presupposes that an economic agent (producer, consumer) has a certain set of rights that guarantee him autonomous, independent decision-making. However, economic freedom is also a source of uncertainty, since the freedom of one economic agent is simultaneously accompanied by the freedom of others.

Risks are a formalization of uncertainty, and the definition of risks is a way of measuring it. After all, despite the fact that the feeling of uncertainty is almost always unpleasant, in some cases it causes more inconvenience, in others less. Reducing uncertainty means reducing the number of risks, where everything is clear and transparent there are no and cannot be risks. But a situation of “complete uncertainty” is very rare in our world. Perhaps due to the fact that risks are closely related to uncertainty, there are many interpretations of the concept of “risk”. According to some definitions, risk is the danger of a negative event occurring; according to others, it is damage due to negative events; yet another interpretation calls risk the probability of something occurring, both negative and positive, etc. There is especially a lot of discussion surrounding the definition of risk as a necessarily negative event. After all, positive but unplanned events are usually not considered risks.

Indeed, risk is characterized by the probability of the occurrence of some event and implies, if not danger, then at least the impact of this event on business, life, project, etc. In domestic economic science, there are essentially no generally accepted theoretical provisions on business risk; in fact, methods for assessing risk in relation to certain production situations and types of business activity have not been developed; there are no recommendations on ways and means of reducing and preventing risk.

Of particular interest is a comparative examination of the classical and neoclassical theories of entrepreneurial risk and their economic applications. When studying entrepreneurial profit, such representatives of the classical theory as J. Mill, I.W. Seniors distinguished in the structure of entrepreneurial income a percentage (as a share of the invested capital), an entrepreneur’s wages and a risk fee (as compensation for the possible risk associated with entrepreneurial activity). In the classical theory of entrepreneurial risk, the latter is identified with the mathematical expectation of losses that may occur as a result of the chosen decision. The risk here is nothing more than the damage that is caused by the implementation of this decision.

This one-sided interpretation of the essence of risk caused sharp objections among some foreign economists, which led to the development of a different understanding of the content of business risk.

In the 30s of our century, economists A. Marshall and A. Pigou developed the foundations of the neoclassical theory of entrepreneurial risk. The basics of this theory are as follows: an entrepreneur working in conditions of uncertainty and whose profit is a random variable is guided by two criteria when concluding a transaction:

* the size of the expected profit;

* the magnitude of its possible fluctuations.

The behavior of an entrepreneur, according to the neoclassical theory of risk, is determined by the concept of marginal utility. This means that if there are two options, for example, capital investments that give the same expected profit, the entrepreneur chooses the option in which the fluctuations in expected profit are smaller. According to neoclassical theory, for an entrepreneur, a certain profit of the same expected size, but associated with possible fluctuations, is less interesting. The problem of risk in our country is quite mature. The formation of market relations in Russia was a prerequisite for a more in-depth development of risk theory in the domestic economic literature. Fundamental for all modern definitions of risk in Russian science is the interpretation in the famous dictionary by S.I. Ozhegova. So, risk, according to Ozhegov’s dictionary, is “the action of failure, in the hope of a happy outcome...”. More specifically, this is:

Action, activity as a condition for the emergence of risk;

Action at random, in other words, is activity without preliminary calculation, with the hope of a favorable event, or goal-setting, goal-fulfilling activity;

Activity “in the hope of a happy outcome” - we are not talking about any activity, but about one that satisfies needs; based on them, setting goals and predicting a successful result.

In fact, the definition of risk in Russian and foreign literature can be combined into the following groups. The first group includes definitions in which risk is understood as a probability that deviates from the planned results. In the second group, the emphasis is on the possibility of quantitative or qualitative risk assessment.

In the third group, the concept of “risk” is revealed through the activity of the subject: action “at random” in the hope of a happy outcome: a mode of action in an unclear, uncertain situation; choosing alternatives in a situation of uncertainty, realizing the ability to creatively use the element of uncertainty. From the above, it should be concluded that risk is, first of all, a set of events, and it has a set (discrete or continuous) of its implementation, each of which has its own probability and amount of damage. A chain of successive steps leading to the final, main event is a script. Risk situations themselves generally have such features as rarity; uniqueness; continuity; repeatability. A risk situation can have different consequences, i.e. not only losses, but also income and benefits. Therefore, the following risk functions are distinguished:

Regulatory (stimulating): has a contradictory nature and appears in two forms: constructive and destructive. Risk is aimed at obtaining results in an unconventional way. Risk plays the role of a catalyst, for example, when solving innovative, investment problems, which means that the stimulating aspect of risk operates.

The protective function is manifested in the fact that, since risk is a stable state of the economic system, social protection, legal, political and economic guarantees are needed that exclude punishment in cases of failure and stimulate justifiable risk.

Risk performs an innovative function by stimulating the search for unconventional solutions to problems facing an economic entity.

The analytical function of risk is related to the fact that the presence of risk presupposes the need to choose one of the possible decision options, and therefore the economic entity analyzes all possible alternatives in the decision-making process.

Thus, risks are a complex dynamic category and therefore need to be assessed in all activities.

1.2 Classification and methods of risk assessment in enterprise activities

The composition of risks considered in economic research is closely related to the characteristics of business activity and the environment in which it is carried out.

The scientific literature uses a number of well-defined principles that can be used as a basis for classifying risks and accordingly used in developing strategies to protect against them.

Various methods and tools are used in risk management, so a scientifically based classification is needed that will systematize risks and identify specific areas for their reduction or optimization.

Risk classification refers to the distribution of risks into specific groups in accordance with certain general characteristics and to achieve set goals. A scientifically based risk classification helps to clearly define the place of each risk in the system and creates potential opportunities for the effective use of appropriate methods and risk management techniques.

In the economic literature studying risks and related problems, there is no single coherent system for their classification. In different classifications, risks are detailed in different ways, divided into groups, etc. We can safely say that there are even more classifications of risks than definitions of risks. In a number of works by domestic authors, such as V. Abchuk, A. Algin, G. Kleiner, V. Severuk, B. Raizberg, V. Rotar, I. Shumperi, etc., there are radically different approaches to risk classification. Some distinguish two types of risks: the risk associated with possible technical failure of production, and the risk caused by commercial success. Yu. Osipov considers three types of business risk: inflationary, financial and operational.

The most important features underlying risk classification are the following:

Time of occurrence;

Main factors of occurrence;

Nature of accounting and consequences;

Sphere of origin.

In the work of I.T. Balabanwa “Risk Management” proposes a hierarchical system for classifying economic risks, schematically presented in Figure 1.1, the structure of which includes groups, categories, types, subtypes and varieties of risks. In accordance with the presented hierarchy, depending on the possible result, risks are pure and speculative... and if pure risks lead to the possibility of obtaining a negative or zero result, then speculative risks are expressed by the possibility of obtaining both positive and negative results.

Rice. 1.1 Hierarchical risk classification system

As for foreign practice, the famous economist John Keynes was one of the first to propose a classification of risks; he considered three categories of risks and, most likely, did this as part of a global study of the general theory of employment, interest and money:

· Entrepreneurial risk - the risk of not receiving the expected income from an investment;

· “Lender” risk - the risk of non-repayment of a loan, including legal (evasion of loan repayment) and credit risk (insufficient collateral);

· Risk of changes in the value of a monetary unit - the probability of losing funds as a result of changes in the exchange rate of the national currency.

Credit and legal risk are present in all classifications.

Let's consider the main types of risks according to various classification criteria.

Commercial risk is associated with the danger of losses in the process of financial and economic activity. Based on their structural characteristics, commercial risks are divided into:

A) on property risks associated with the likelihood of loss of property of a citizen or entrepreneur due to collapse, sabotage, negligence, overstrain of technical and technological load on equipment;

B) production risks associated with losses from stopping the enterprise as a result of the influence of various factors, and above all with damage or disposal of fixed and working capital;

C) trade risks associated with losses due to delays in payments for goods and services, non-delivery of goods, refusal of payments during the transportation of goods, etc.;

D) financial risks associated with the purchasing power of money, investment of capital, and the likelihood of loss of financial resources.

Financial risks include:

· Inflation risk is an increase in the price level as a result of the overfilling of monetary circulation channels with excess money supply in excess of the needs of trade turnover, as a result of which monetary incomes depreciate in terms of purchasing power faster than they grow;

· Deflationary risk is the risk that with an increase in the purchasing power of money, a fall in the price level occurs, a deterioration in the economic conditions of business and a decrease in income;

· Currency risk - a risk caused by the danger of losses associated with changes in the exchange rate of foreign currencies in relation to the national currency during foreign trade, credit, and foreign exchange transactions on stock and commodity exchanges. Currency risk includes operational risks (the risk of loss of profit caused by unfavorable changes in the exchange rate) and translational risks (associated with changes in the price of assets and liabilities in foreign currency caused by fluctuations in exchange rates.)

· Liquidity risk - associated with the possibility of losses when selling securities or other goods due to changes in quality assessment;

· Investment risk - associated with lost profits, as well as a decrease in profitability, and the danger of non-payment of debt.

The risk of a decrease in profitability is a type of investment risk that may arise as a result of a decrease in the amount of interest and dividends on portfolio investments, deposits and loans. It includes the following types of risks:

· interest rate risk - the danger of losses by commercial banks, credit institutions, investment institutions, companies as a result of the excess of the interest rates they pay on borrowed funds over the rate on loans provided.

· price risk - the risk of changes in the price of a debt obligation due to a rise or fall in interest rates;

· credit risk - the risk associated with the risk of non-payment by the borrower of the principal debt and interest due to the lender. Credit risk is associated with property risk - this is the risk in a credit transaction associated with the condition or quality of the lender's property.

The risk of direct financial losses includes:

stock exchange risk;

· selective risk;

· risk of bankruptcy.

However, there are other types of risks.

Contagion risk - the risk that the problems of subsidiaries and associated companies will spread to the parent company, and vice versa.

Uninsurable risks are risks the probability of which is difficult to calculate even in the most general form and which are considered too great for insurance.

As well as tax risk, organizational, innovation, industry, external and internal, regional risks.

Given the variety of risks, assessing the damage to an object from an adverse event is the most difficult problem, since in practice it is usually not possible to obtain unambiguous and universally accepted values. Moreover, risk theory, as a rule, deals with expected damage given the assumed known force, nature of the event and the degree of protection of the object. From this remark, an important conclusion for the theory and practice of risk analysis follows: “absolutely objective and unambiguous assessments of damage cannot be obtained in the vast majority of situations.” Often, damage indicators used outside the framework of economic and legal relations of risk analysis in a particular area of activity can be considered economically meaningless.

Usually, when developing a method for calculating damage that is expected to be widely used in practice, they try to take into account a certain set of minimum requirements. These include:

1. simplicity in terms of application.

2. Focus on the minimum amount of initial information.

3. Taking into account the features of the object.

4. Taking into account as many losses as possible without significantly complicating the calculations.

5. Taking into account the patterns of changes in the nature and extent of damage over time, taking into account the changing force of impact

6. Compliance of damage assessments with economic and legal relations existing in the state and regions and a number of others.

In order to bring together the positions of different subjects, they usually try to structure its overall value by dividing it into relatively independent elements, for each of which assessment methods adequate to their content can be used. For example, it is advisable to divide damage by recipients (objects of impact): by regions, enterprises, buildings, structures, equipment. The total amount of damage in such a situation can be obtained by summing up the damage of individual independent groups of recipients, which in turn can be divided according to the location and time of occurrence of events, direct and indirect.

Direct damage usually refers to losses directly caused by the occurrence of events. Examples of them are losses of material assets during an earthquake, a decrease in the value of shares due to the crisis, and loss of capital due to the default of borrowers.

Indirect damage characterizes losses caused by unfavorable changes in the external and internal environment.

In general, the entire set of methods for assessing economic damage to an object can be divided into three main groups: the direct counting method (reflects all the elements in the chain of cause-and-effect relationships. It is assumed that the effects that arise between all the information in this chain and the calculation of the various components of loss items for the object are assessed) ; methods of indirect assessment (based on some assumptions regarding the patterns of damage formation.); combined methods (various combinations, combinations of methods that complement each other in solving individual problems of assessing damage from risk).

1.3 Management of risks

In the risk management system, an important role is played by the correct choice of measures to prevent and minimize risk, which largely determine its effectiveness. The risk reduction system includes certain methods and ways:

1. Obtaining comprehensive information about the upcoming choice and result.

2. Risk avoidance.

3. Diversification.

4. Reserving funds to cover unforeseen expenses.

5. Limitation.

6. Hedging.

7. Risk insurance, self-insurance.

8. Checking business partners and terms of the transaction. Business planning.

9. Recruitment of personnel for a business organization.

10. Transfer of risk.

11. Other methods.

The choice of a particular risk minimization method above depends on the experience and capabilities of the entrepreneur and any other manager. For a more effective result, a combination of methods is usually used.

In his activities, a manager encounters many risks, therefore, in addition to the basic methods of minimizing them, he uses specific methods that are used only in this case. Ways to minimize the most common risks are given in Table 1.2. (Appendix 2)

Indeed, actions aimed at mitigating risk can be very different. People enroll in extreme driving courses to reduce the likelihood of getting into an accident in difficult conditions - this is also a strategy for mitigating, minimizing, eliminating risk. The choice of one method or another depends on the specific situation, the degree of risk and the capabilities of the enterprise. This is what determines the fundamental decision: accept the risk, reducing its negative consequences using various methods, or avoid it.

In the process of carrying out business activities, a company may refuse to carry out financial transactions or activities associated with a high level of risk. This direction of risk neutralization is the simplest and most radical; it will completely avoid potential losses, but does not at all contribute to obtaining profits associated with risky activities.

When concluding any transaction, to reduce the risk of business contracts, the entrepreneur needs to check the prospective partner. The basic rule of business is “trust, but verify.” A possible way to avoid mistakes when choosing a partner is to create your own system for collecting and analyzing information about potential or existing counterparties. As an example in this case, you can use the Due Diligence system practiced by Western banks in relation to their clients. This system provides protection against various types of fraud. One of the main tools of such a system is a questionnaire, including questions about the name of the counterparty company and the addresses of its offices for the last two to three years; about the types of business it carries out. The questionnaire may contain questions about the company's partners and their addresses, it includes questions about the financial condition of the company and the expected turnover or future average account balance. The most difficult questions in the questionnaire are related to the origin of the company's capital. Such a questionnaire provides preliminary information about the client, and if something in his answers is alarming, additional research should be carried out, including a search for confirmation (or refutation) of the data received, a search for facts that the partner has kept silent about, as well as checking information through others counterparties.

Risk diversification is perhaps the most complex and interesting risk management method that requires high professionalism. It represents the use of the economic and mathematical concept of “negative correlation” in economic practice. Invested funds are directed to completely independent transactions and projects that are in no way related to each other. In this case, if a risk event occurs and losses occur on one transaction, you can count on a successful and profitable outcome of another. Moreover, it is advisable to focus on negatively correlated outcomes, that is, to choose investment values (objects) with directly opposite profitability vectors. Then profits on one transaction will be able to compensate for possible losses on another.

When forming a securities portfolio, the problem of risk diversification is given particularly serious attention. First of all, the “rule of a dozen” applies. It is necessary to ensure a sufficient variety of securities. Therefore, generally accepted practice dictates that a bank’s portfolio should contain at least twelve blocks of shares in a wide variety of companies. Next, pay attention to the level of profitability and degree of risk of the securities. High-yield securities typically involve a considerable degree of risk. Securities with acceptable risk yield correspondingly very moderate returns. And low-risk securities are ineffective and not interesting for the bank. The “five finger rule” offers a way out of this situation. It follows from it that to form an optimal portfolio, out of every five shares, one should be low-risk, three should be with normal, acceptable risk, and one should be high-risk, but also high-yielding.

In addition, the financial sector of the economy often uses a method of risk diversification, called “risk hedging.” Risk hedging involves limiting the amount of losses with financial instruments, but as a consequence, profits too. It is carried out in the form of concluding parallel financial compensation transactions, when a possible loss on one transaction is compensated by a possible profit on another. There are many ways to hedge risks, but the main, most used and frequently encountered are options, futures and swap transactions.

The next step in solving the problem of risk management is to study the possibility of full or partial self-insurance of the transaction. Self-insurance is nothing more than taking risks on oneself and, undoubtedly, is the cheapest (with the possible exception of renouncing risks) way of dealing with risks. It is assumed that possible damage will be covered with current funds or with the help of a reserve fund. Therefore, it is obvious that the use of self-insurance opportunities is very limited. Basically, this method is justified if the probability of a negative outcome and the amount of possible loss are not large.

When using self-insurance, you need to be aware that the cost-effectiveness of this method results in some negative aspects. First of all, this is the “death” of working capital. The company is forced to keep considerable funds in reserve; they cannot be counted on when concluding new, often interesting and effective contracts; it is impossible and dangerous to put them into circulation. However, there is still a danger that there will be a “streak of failures”: against the backdrop of low financial income, losses will occur one after another in a short period of time, and any reserve funds will still not be enough. All this causes uncertainty and nervousness among management, which will certainly be transmitted to the entire staff of the company. If loss prevention and self-insurance do not provide the desired protection against risk and only slightly reduce it, which is quite likely in modern business, one can apply the most common and widely used, already traditional method of risk management, which is insurance. The essence of this method is that the entrepreneur takes an insurance company as a partner in the transaction and assigns to it, after concluding the appropriate contract and paying insurance premiums, a significant part of the expected risks. Unlike all industries and spheres of the economy, where risk for an entrepreneur is an undesirable side effect, in the insurance business risks serve as the main field of activity. That is, the risks of the entrepreneur are assumed by the professional.

When deciding to use insurance, you need to keep in mind that, firstly, the risk must be random in nature, a negative outcome should not be pre-programmed and included in the transaction. Secondly, only losses that can be measured and assessed using natural and monetary indicators are insured. And finally, the risk itself cannot be the object of insurance. Such an object is the company’s inventory and cash assets [21, p.65].

Let us note that economic risks are an inevitable component of business activity, since they are immanent in the market. Risks cannot be eliminated, but it is quite possible to reduce possible losses. This can be achieved through the application of risk management techniques. Of course, risk management is associated with certain costs for the company, but its implementation is necessary and justified. By managing risk, a firm sacrifices less to save more. It replaces the possible occurrence of significant losses with relatively small, strictly defined costs of risk management.

2. Analysis of risks in the activities of the enterprise JSC Galantus

2.1 Technical and economic characteristics of JSC Galantus

JSC "Galantus" dates back to January 7, 1979, when the state farm "Ornamental Crops" began its activities on the basis of "Zelenstroy". The main industrial crops were roses, carnations, seedlings for landscaping, and potted crops. The bulk of the protected ground area was made up of glass greenhouses with a total area of about 3000 square meters. m.

The main reconstruction of the farm began in 1988 and was associated with the construction of new greenhouses that meet modern floriculture standards, with an area of more than 31,000 square meters. m., the construction of a new powerful boiler house and a complete change in the technology of growing flower crops. The introduction of modern technology from leading companies in the world has made it possible to make a huge qualitative and quantitative leap in increasing production. Over the past ten years alone, gross income from flower production has increased more than 10 times, profit - 8 times, average monthly wage - 5 times.

On August 28, 1994, the state farm was reorganized into the joint-stock company "Galantus". Translated into Russian, “galanthus” means “snowdrop”.

Today, the company’s activities are well known to flower growers in Russia and abroad. JSC "Galantus" is a farm that meets world standards of floriculture, using modern technology and equipment. The total area of protected soil is 4.2 hectares. More than 5 million cut flowers are grown annually in this area.

A professional florist today is interested in new crops and varieties that are highly rated in Europe, adapted to Russian conditions and provide good business in the flower market.

Accounting at JSC "Galantus" is carried out in accordance with the standard chart of accounts for accounting of financial and economic activities of enterprises; standard forms of financial statements and instructions for their use and completion; other legal acts regulating the accounting of transactions. When carrying out activities, the forms of documents determined by the albums of unified forms of primary accounting documentation developed by the republican governing bodies are used. Documents whose forms are not provided in these albums contain mandatory details in accordance with current legislation. The features of accounting at JSC Galantus are summarized in the Order on Accounting Policy, which is annually approved by the General Director of JSC Galantus. The accounting policy determines the organization of document flow, the procedure for processing information (using accounting registers), the procedure for conducting inventory, etc. The balance sheet of the enterprise is presented in Appendix 1. Open joint-stock company "Galantus", according to current legislation, is recognized as a limited liability company, which operates on the basis Charter and legislation of the Russian Federation.

Table 2.1 Main economic indicators of JSC Galantus

|

Indicators |

Change (+,-) |

Growth rate, % |

|||

|

1. Sales revenue, thousand rubles. |

|||||

|

2. Cost of goods sold, thousand rubles. |

|||||

|

3. Administrative and commercial expenses, thousand rubles. |

|||||

|

4. Profit from sale, thousand rubles. |

|||||

|

5. Profit up to taxation, thousand rubles |

|||||

|

6. Net profit, thousand rubles. |

|||||

|

7. Cost fixed assets, thousand rubles |

- -1154*91,90 -136273147 ¦ |

||||

|

8. Value of assets, thousand rubles. |

|||||

|

9. Own capital, thousand rubles. |

|||||

|

10. Borrowed capital, thousand rubles. |

|||||

|

11. Number of teaching staff, people. |

|||||

|

12.Labor productivity, thousand rubles. (1/11) |

|||||

|

13. Capital productivity, rub. (1/7) |

|||||

|

14. Asset turnover, times (1/8) |

|||||

|

15. Return on equity on net profit, % (6/9)*100% |

|||||

|

16. Sales profitability, % (4/1)*100% |

|||||

|

17. Return on equity on profit before tax, % (5/(9+10))*100% |

43947/(336039+64841)=43947/400880=10,9% |

52049/(363590+134467)=52049/498057=10,5% |

|||

|

18. Costs per ruble of sales proceeds, ((2 + 3)/1)*100 kop. |

Having analyzed the obtained indicators, we can draw conclusions and build diagrams based on the most significant indicators.

In diagram 2.1 we can clearly see the difference in sales revenue for 2010 and 2011. Sales revenue is a regular source of income for the organization from all possible receipts of funds, serves as the main evaluative indicator of the enterprise's performance; by its receipt one can judge that the products sold in terms of volume, quality and do not correspond to market demand, since during the period under review it decreased sharply.

Diagram 2.1. Sales proceeds

Having examined the following indicator - the cost of goods sold (Diagram 2.2), we see that sales revenue at JSC Galantus fell not due to quality or lack of demand, but due to a sharp reduction in production capacity and the volume of goods produced.

Diagram 2.2. Cost of goods sold

When considering the profit from sales indicator (Diagram 2.3), one can notice a significant increase in this indicator in 2011.

Diagram 2.3. Profit from sale

Also, according to the balance sheet data, one can notice that in 2011 the company OJSC Galantus significantly increased the amount of borrowed funds compared to the previous year. (Diagram 2.4)

Diagram 2.4 Borrowed capital

The company OJSC "Galantus" reduced sales volume and reduced production costs by purchasing cheap quality resources, thereby increasing the profit from sales, and the company also took out a large loan, we can conclude that the company is going to invest all its funds in some profitable project (any changes in the production structure) expand your production, or change the specification

2.2 Risk assessment in the activities of JSC Galantus

The main objective of the methodology for determining the degree of risk is to systematize and develop an integrated approach to determining the degree of risk affecting the financial and economic activities of the enterprise.

The financial statements of the enterprise are used as initial information when assessing financial risks: a balance sheet that records the property and financial position of the organization as of the reporting date; An income statement presenting the results of operations for an accounting period.

The central place in assessing business risk is occupied by the analysis and forecasting of possible losses of resources when carrying out business activities.

Quantitative risk assessments, in this work we will consider an investment project, are associated with the numerical determination of individual risks and the risk of the project as a whole. The task of quantitative analysis is to numerically measure the degree of influence of changes in risk factors of the project, tested for risk, on the behavior of the project performance criteria.

The company OJSC Galantus has been conducting investment activities for many years. And for 2013, the company has two investment options. It has been established that when investing capital in enterprise A, receiving a profit in the amount of 250 thousand rubles has a probability of 0.6, and in event B - receiving a profit in the amount of 300 thousand rubles. - probability 0.4. then the expected profit from investing capital (mathematical expectation) will be 6

For event A - 150 thousand rubles (250 * 0.6);

For event B - 120 thousand rubles (300 * 0.4);

The probability of an event occurring can be determined by an objective or subjective method. Using an objective method, we will obtain a determination of probability based on a calculation of the frequency with which a given event occurs. Investment of capital in event A profit in the amount of 250 thousand rubles. was obtained in 120 cases out of 200, the probability of such a profit will be about.6 (120:200).

An important place in this regard is occupied by expert assessment, i.e. conducting an examination, processing and using its results in justifying the value of probability. Here the degree of risk is measured according to two criteria:

The average expected value (MEV) is the value of the magnitude of the event. Is a weighted average of all possible outcomes;

Fluctuations in possible results.

Thanks to the data provided by the statistical department, we know that when investing capital in event A, out of 120 cases, the profit is 250 thousand rubles. was obtained in 48 cases (probability 0.4), a profit of 200 thousand. rub. was received in 36 cases (probability 0.3) and a profit of 300 thousand rubles. was obtained in 36 cases (probability 0.3), then:

POP = (250*0.4+200*0.3+300*0.3) = 250 thousand. rub.

Similarly, it was found that when investing in activity B, the average profit was:

POP = (400*0.3+300*0.5+150*0.2) = 300 thousand rubles.

Comparing two amounts of expected profit when investing capital in event A and B, we can conclude that when investing in event A, the amount of profit received ranges from 200 to 300 thousand rubles. and the average value is 250 thousand rubles; when investing capital in event B, the amount of profit received ranges from 150 to 400 and the average value is 300 thousand rubles. But we know that the average value is a generalized quantitative characteristic and will not allow us to make a decision in favor of any result. To make a final decision, it is necessary to measure the variability of indicators (KP), i.e. determine the degree of variability of a possible result.

To do this, we use two closely related values:

· Dispersion (formula 2.1) is the weighted average of the squared deviations of actual results from the average expected ones.

formula 2.1

where is the dispersion;

X- expected value for each observation case;

Average expected value;

n is the number of observation cases (frequency).

The calculation of variances for activities A and B is presented in Table 2.1.

Table 2.1. Calculations of variances when investing capital in activities A and B

|

Event no. |

Profit received, thousand rubles. |

Number of cases observed |

(- ) |

|||

|

Event A |

||||||

|

Total = |

||||||

|

Event B |

||||||

|

Total = |

The coefficient of variation (V) is usually used for analysis. It represents the ratio of the standard deviation to the arithmetic mean and shows the degree of deviation of the obtained values. CV can vary from 0 to 100%. The higher the CV, the stronger the oscillation. The following qualitative assessment of various EFs has been established:

Lo 10% - weak fluctuation;

10-25: - moderate;

Over 25% - high.

Let's calculate the standard deviation when investing capital in activity A. It will be:

180000/120 = 38,7;

For event B:

750000/100= 86,6;

Let's calculate the coefficient of variation for activity A:

V = 38.7/250*100=15.5%;

Coefficient of variation for activity B:

V=86.6/300*100=29.8%

According to the calculation data, we can see that the coefficient of variation when investing capital in event A is less than when investing in event B, which allows us to conclude that a decision has been made in favor of investing capital in event A.

3. Ways to reduce and manage risks at JSC Galantus

Having examined the main technical and economic indicators of Galantus OJSC, we found that revenue from the sale of products in 2011 compared to 2010 decreased by 93% as a result of rising product prices; despite the fact that the cost of products sold decreased by 87.7%, this growth does not have a significant impact on net profit, but in general, such indicators are a negative trend in the work of the enterprise.

The value of current assets in 2010 increased by 124%, which is associated with taking out a loan of 72,000 rubles.

In 2011, an increase in current assets by 124% was due to an almost sixfold increase in accounts receivable.

The amount of equity in 2011 increased by 108% respectively as a result of an increase in retained earnings.

The decrease in borrowed capital in 2010 is associated with a decrease in short-term loans and borrowings and the share of accounts payable, and the increase in 2011 is due to an increase in short-term loans and borrowings by 207%.

Having analyzed the absolute indicators of financial stability, we conclude that in 2009 and 2010 the enterprise belonged to the fourth type of financial stability, i.e. it was in a financial crisis, in which it was threatened with bankruptcy, and in 2011 the company was in an unstable financial position, which is characterized by insolvency, but it already belonged to the third type of financial stability.

After analyzing the solvency, it was revealed that the company does not have absolute liquidity, this indicates that the solvency of the organization is at a low level. After an analysis of the financial condition and risks, it was revealed that Galantus OJSC has a high risk of bankruptcy, since it is in an unstable financial position.

Therefore, the measures we have discussed for investing assets can improve your financial condition.

Financial stabilization at an enterprise in a crisis situation is consistently carried out in two stages:

1) elimination of insolvency;

2) restoration of financial stability.

The essence of restoring solvency is to maneuver cash flows to restore the balance between their expenditure and receipt.

The essence of restoring financial stability is the fastest and most radical reduction in ineffective expenses. Stopping unprofitable production is the first step that needs to be taken. If unprofitable production is not practical or cannot be sold, it must be stopped to immediately prevent further losses.

Conclusion

Man constantly faces risk. Often, without complete information, we have to make a choice, which, unfortunately, is not always the right one. Any entrepreneur always acts at his own peril and risk; the further activities of the organization will depend on this person, on his foresight and knowledge. One of its main tasks is to assess risk and reduce it to a minimum in order to obtain maximum profit in the event of a successful transaction and incur minimal losses in the event of an unsuccessful transaction. By incorrectly determining the influence of certain factors, a manager can lead the company to collapse. Therefore, the importance of such qualities as experience, qualifications, and, of course, intuition increases sharply. A constant analysis of the existing situation is necessary; it is very important to use the experience of other organizations (the opportunity to learn from other people’s mistakes).

At the same time, all approaches are characterized by a single goal: it is necessary to assess the levels of risks inherent in certain types of activities and develop effective measures that can reduce these levels to acceptable values. The similarity of goals in this case predetermines a unified methodology for solving these problems - the methodology of risk analysis.

Risk management, in general, should be considered as one of the activities aimed at increasing the sustainability and safety of an object, the efficiency of its functioning and development.

The main difficulty of risk management is that there are no “ready-made” recipes. Each issue that needs to be addressed in an enterprise requires its own unique approach.

Bibliography

1.The Constitution of the Russian Federation of December 12, 1993. Official publication of M.; 2012

2. Tax Code of the Russian Federation dated July 19, 2000. Official publication M.: M 2012.

3.Civil Code of the Russian Federation dated December 18, 2006 N 230-FZ

4.Federal Law No. 14 of 02/08/1998 “On Limited Liability Companies

5. Balabanov I.T. Risk management. -M.: Finance and Statistics. 2006.

6.Blank I.A. Financial risk management: Textbook. well. - K.: Nika-Center, 2006.

7. Brolio E. System for assessing the risks of innovative activity of an organization / E. Brolio. Problems of management theory and practice, 2008. No. 4

8. Vasin S.M. Risk management in an enterprise: a textbook - M.: KNORUS, 2012

9. Vishnyakov Ya.D. General theory of risks. M.: "Academy", 2007

10. Granaturov V. M. Economic risk. Essence, measurement methods, ways to reduce. - 2011

11. Delyagin M. How to overcome the crisis yourself. The science of saving, the science of taking risks. Simple tips. - 2009

12. Kudryavtsev A. A.. Integrated risk management - 2010

13. Lapchenko D.A. Assessment and management of economic risk: theory and practice. Minsk: Amalfeya, 2007.

14.Lobanova A.A. Encyclopedia of financial risk management. M.: Alpina, 2005.

15. Nikonov V. Risk management: How to earn more and spend less. - M.: Alpina Publishers, 2009

16. Polovinkin L., Zozulyuk A. Entrepreneurial risks and their management // Russian Economic Journal. - 2004. - No. 9.

17.Making financial decisions: theory and practice / ed. A.O. Levkovich. - Minsk: Grevtsov Publishing House, 2007.

18. Serebryakova T. Yu.. Risks of the organization and internal economic control. - 2011

19. Tikhomirov N.P. Risk analysis in economics. - M.: JSC "Economy", 2010

20. Uspensky V.A. risk management methods / Nota Bene - Economic online journal - Articles Archive

21. Fomichev A.N. “Risk Management” M.: Dashkov i K 2004.

22. Tsvetkova E. V., I. O. Arlyukova. Risks in economic activity. Training manual.- 2005

23. Chetyrkin E.M. Financial mathematics: Textbook. - 6th ed., rev. - M.: Delo, 2006.

24. Shapkin A. S., Shapkin V. A. Economic and financial risks. Valuation, management, investment portfolio - 2010.

25. Shvandar V.A. Risks in the economy: Textbook. manual for universities / Ed. prof. V.A. Shvandara. - M.: UNITY-DANA, 2007

Annex 1

Appendix 2

Table 1.2. Ways to minimize risks

|

Type of risk |

Ways to reduce risk |

|

|

Commercial risk |

Correctly determine and maintain the ratios of financial indicators; increase the ROI of your business |

|

|

Financial risk |

Timely place passive funds in profit-generating projects or provide loans |

|

|

Manager errors |

Introduce control and duplication at the key links of the business |

|

|

Squeak of the wrong selected project |

Carefully check all the pros and cons, if necessary, use computer modeling to accurately calculate all options |

|

|

Economic fluctuations and changes in demand |

Fluctuations and changes in demand must be predicted and used in business plans |

|

|

Risk of suboptimal resource allocation |

Clearly define priorities in resource allocation depending on the planned number of products produced |

|

|

Actions of competitors |

Possible actions of competitors must be anticipated based on a systematic analysis of their activities |

|

|

Employee dissatisfaction |

Carefully consider social and economic programs for employees, taking into account their requirements and requests. Create a favorable environment in the team |

|

|

Low volumes of goods sales |

Conduct thorough analytical work to select target markets |

|

|

Risk of information leakage |

Careful screening and selection of employees, especially scientific and technical personnel |

Posted on Allbest.ru

Similar documents

Methods and tools for analyzing risks of the financial and economic activities of an enterprise. Assessment of financial and economic activities of PSC TAIF-NK. Analysis of the risk of bankruptcy based on foreign models. Mechanisms for neutralizing financial risks.

thesis, added 11/11/2010

Theoretical foundations of the concept, signs and classification of risks. Basic methods of risk management. Analysis of the financial condition of the enterprise taking into account the risk factor. Selecting measures to reduce risks. Evaluating the effectiveness of proposed activities.

course work, added 12/23/2014

Development of measures to reduce risks at the enterprise. The concept of risk and its economic content. Analysis of business risks of TPPUP "Seafood Service". Ways to improve the efficiency of the risk management mechanism. Creation of a risk management department.

thesis, added 06/26/2010

The essence and role of risks in the activities of an enterprise. Classification and types of risks of oil and gas enterprises. Analysis and assessment of the effectiveness of the risk management system at Shell LLC, ways to improve it. Control of certain risks in the activities of Shell LLC.

thesis, added 06/30/2012

Concept, classification and types of risks in the foreign economic activity of an enterprise. The main directions of foreign economic activity of LLC "EL". Recommendations for the implementation of a risk transfer system (insurance and outsourcing) in logistics operations.

thesis, added 07/02/2015

Classification of production, investment risks and risks of trading activities of an enterprise. Characteristics of statistical methods used in qualitative and quantitative risk analysis. Calculation of variance and standard deviation.

lecture, added 02/13/2011

Determining the specifics of innovation risks. Methods for reducing the risks of innovation. Examination of an idea, commercial proposal or project as a whole. Risk assessment of an innovation project and development of a risk management mechanism.

course work, added 03/22/2016

The concept of risk management in business. The economic nature of the risks of foreign economic activity in Ukraine, their classification and analysis. Methodology for assessing the risks of foreign economic contracts and production activities.

thesis, added 12/10/2009

Identification and assessment of risks affecting the shareholder value and investment attractiveness of IDGC of Siberia, JSC. Core business risk management policy. An approach to determining decision threshold levels for risk management.

thesis, added 10/15/2015

Documents regulating the activities of a commercial organization. General principles of business risk analysis. Qualitative and quantitative risk analysis of commercial organizations. Determining the level of risk of loss of marginal profit.

In an era of economic and financial crisis, risk management is the most pressing problem facing Russian industrial companies. Globalization processes are becoming another source of economic risks, so the use of risk management principles in management will contribute to achieving the goals and objectives of chemical companies, although, of course, it will not reduce the likelihood of various types of risks to zero.

The introduction of a risk management system at enterprises makes it possible to:

- identify possible risks at all stages of activity;

- predict, compare and analyze emerging risks;

- develop the necessary management strategy and complex decision-making to minimize and eliminate risks;

- create the conditions necessary for the implementation of the developed activities;

- monitor the operation of the risk management system;

- analyze and monitor the results obtained.

The features of risk management include: the need for company management to have advanced thinking, intuition and foresight of the situation; the possibility of formalizing the risk management system; the ability to quickly respond and identify ways to improve the functioning of the organization, reducing the likelihood of undesirable events.

Comprehensive risk management system ERM (Enterprise Risk Management) in many foreign companies, for example, in the USA, is already used quite widely, since the owners of large global companies have already seen in practice that old management methods do not correspond to modern market conditions and are not able to ensure the successful development of their business.

The application of risk management presupposes a clear distribution of responsibilities and powers between all structural divisions. It is the responsibility of senior management to appoint those responsible for implementing the necessary risk management procedures at all levels. Such decisions must comply with the strategic goals and objectives of the company and not violate the terms of current legislation. In this case, it is necessary to correctly distribute among the performers the activities for identifying risks and the functions of monitoring the created risk situation.

Risk management as a key tool aimed at improving business efficiency

Risk management is one of the key tools aimed at improving the effectiveness of business management programs, which they can use to reduce product life cycle costs and mitigate or avoid potential problems that could interfere with the success of the business.

Achieving the goals of an enterprise requires specific ideas about the main type of activity, production technologies, as well as the study of the main types of risks. Preventing risks and reducing losses from exposure leads to sustainable development of the enterprise. The process by which the activities of an enterprise are directed and coordinated from the point of view of the effectiveness of risk management and represents risk management. Risk management is the process of identifying the losses that an organization faces in its core activities and the extent of their impact, and selecting the most appropriate method to manage each individual risk.

In another view, risk management is a systematic process in which risks are assessed and analyzed to reduce or eliminate their consequences, as well as to achieve goals.

Based on the above, we can come to the conclusion that risk management to ensure the viability and efficiency of the enterprise is a cyclical and continuous process that coordinates and directs the main activities. This should be done through the identification, control and mitigation of all types of risks, including monitoring, communication and consultation aimed at meeting the needs of the population, without compromising the ability of future generations to meet their own needs. Risk assessment leads to the stability of the enterprise’s activities, contributing to its sustainable development. Risk management - a contribution to sustainable development, is an essential factor in maintaining and increasing the stable activity of the enterprise. Active risk management is critical to the management process to ensure that risks are being handled at the appropriate level.

Planning and implementing risk management includes the following steps:

- Management of risks;

- identification of risks and the degree of their impact on business processes;

- application of qualitative and quantitative risk analysis;

- development and execution of risk response plans and their implementation;

- monitoring risks and management processes;

- the relationship between risk management and performance;

- assessment of the overall risk management process.

Methodology (program) for continuous risk management

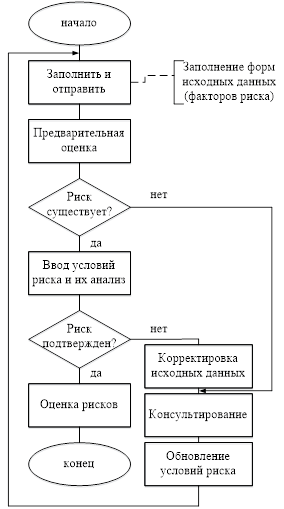

In order to facilitate risk management activities, the enterprise needs to develop a methodology (program) for continuous risk management (CRM). MNUR is a theoretically significant program aimed at developing project management mechanisms with best practice processes, methods and tools for enterprise risk management. It provides the conditions for active decision-making, continuous assessment of risks, determination of the degree of significance and level of influence of risks on management decisions, and the implementation of strategies to combat them. In addition, progress can also be made in the scope of the project, the enterprise budget, the timing of its implementation, etc. Figure 1 clearly illustrates the methodology for the continuous risk management process.

Rice. 1. Continuous risk management process

The performance management process acts as an auxiliary tool for obtaining information necessary for the developed risk management mechanism. Unfavorable trends should be analyzed and their impact on this mechanism assessed. Appropriate actions of the control mechanism must be taken for those areas of activity that are defined as basic in the business processes of the enterprise. Corrective actions may include reallocating resources (facilities, personnel, and rescheduling) or activating a planned mitigation strategy. Severe cases, adverse trends and key indicators can also be taken into account when using this mechanism.

It is important that this mechanism emphasizes the need to reassess identified risks that systematically affect the activities of the enterprise. As the system moves through the development life cycle, most of the information will be available for risk assessment. If the magnitude of the risk changes significantly, approaches to its treatment must be adjusted.

Overall, this progressive approach to risk management is critical to a comprehensive management process and ensures that risk indicators are processed effectively and at the appropriate level.

Development of a risk management program at the enterprise

Let's consider the risk management policy that should be applied at the enterprise. The developed mechanism (program) should be aimed at effective and continuous risk management. Thus, early, accurate and continuous identification and assessment of risks is encouraged, and the creation of informationally transparent risk reporting, planning measures to reduce and prevent changes in external and internal conditions will have a positive impact on the program.

This mechanism, including relationships with counterparties and contractors, should perform the functions of identifying risks and monitoring them. To implement it, it is necessary to have some kind of plan in the form of a set of guidance documents developed for specific areas of activity. This plan sets guidelines for the implementation of MNSD within a specific time frame. It does not affect the conduct of other activities of the entire enterprise, but rather can provide leadership in the area of risk management.

The risk management process must meet a number of requirements: it must be flexible, proactive, and must work towards providing conditions for effective decision-making. Risk management will influence risks by:

- encouraging risk identification;

- decriminalization;

- identifying active risks (continuously assessing what could go wrong);

- identifying opportunities (by constantly assessing the likelihood of favorable or timely occurrences);

- assessing the likelihood of occurrence and severity of impact of each identified risk;

- determining appropriate courses of action to reduce the possible significant impact of risks on the enterprise;

- developing action plans or steps to neutralize the impact of any risk that requires mitigation;

- maintaining ongoing monitoring for emerging risks with a current low impact that may change over time;

- production and dissemination of reliable and timely information;

- promoting communication between all program stakeholders.

The risk management process will be carried out on a flexible basis, taking into account the circumstances of each risk. A core risk management strategy is designed to identify critical areas of risk events, both technical and non-technical, and proactively take the necessary actions to deal with them before they have a significant impact on the enterprise, causing significant costs, reducing product quality or productivity.

Let us consider in more detail the functional elements that are components of the risk management process: identification (detection), analysis, planning and response, as well as monitoring and management. We will consider each functional element below.

- Identification

- Data review (i.e. earned value, critical path analysis, integrated scheduling, Monte Carlo analysis, budgeting, defect and trend analysis, etc.);

- Review of submitted risk identification forms;

- Conducting and assessing risk using brainstorming, individual or group expert assessment

- Conducting an independent assessment of identified risks

- Enter the risk in the risk register

- Risk identification/analysis tools and techniques to be used include:

- Interview techniques to determine risk

- Fault tree analysis

- Historical data

- Lessons Learned

- Risk Management - Checklist

- Individual or group judgment of experts

- Detailed analysis of the work breakdown structure, study of resources and scheduling

- Analysis

- Carrying out a probability assessment - each risk will be assigned a high, medium or low level of probability of occurrence

- Create risk categories – identified risks must be associated with one or more of the following risk categories (e.g. cost, schedule, technical, software, process, etc.)

- Assess the impact of risks - assess the impact of each risk depending on the identified risk categories

- Determining risk severity - assign probabilities and impacts to the rating in each risk category

- Determine the timing when the risk event is likely to occur

- Planning and response

- Risk priorities

- Risk analysis

- Appoint a person responsible for the risk

- Determine an appropriate risk management strategy

- Develop an appropriate risk response plan

- Provide an overview of priorities and determine its level in reporting

- Surveillance and control

- Define reporting formats

- Determine review form and frequency of occurrence for all risk classes

- Risk report based on triggers and categories

- Conducting a risk assessment

- Submission of monthly risk reports

For effective risk management at an enterprise, we consider it advisable to create a risk management department. The main responsibilities of this structural unit, including for staff and other users (including employees, consultants and contractors), in order to successfully implement the risk management strategy and processes are shown in Table. 1.

Table 1 - Risk Management Department Roles and Responsibilities

| Roles | Assigned Responsibilities | |

| Program Director (DP) | supervision of risks of management activities. Monitoring risks and risk response plans. Approval of the decision to finance risk response plans. Monitoring of management decisions. | |

| Project Manager | providing assistance in risk control of management activities Assist in establishing organizational authority for all risk management activities. Timely response to financing risks. | |

| Employee | facilitating the implementation of risk management (the employee is not responsible for the identification of risks, or the success of individual risk response plans). The need to encourage proactive decision-making in determining appropriate risk responses for risk “owners” and department managers. Administer and maintain stakeholder commitment, risk management process Ensuring regular coordination and exchange of risk information between all stakeholders, Management of risks located in a registered risk register (database). Development of knowledge of staff and contractors in the field of risk management activities. | |