What is the law of diminishing marginal productivity? Law of diminishing marginal productivity

Law of diminishing marginal productivity valid in short term and interval when one factor of production remains unchanged. The operation of the law assumes an unchanged state of technology and production technology, if the latest inventions and other technical improvements are applied in the production process, then an increase in output can be achieved using the same production factors. That is, technological progress can change the boundaries of the law.

If a capital is a fixed factor, and work- variable, then the firm can increase production by using more labor resources. But according to the law of diminishing marginal productivity, a consistent increase in a variable resource, while the others remain unchanged, leads to diminishing returns of this factor, that is, to a decrease in the marginal product or marginal productivity of labor. If the hiring of workers continues, then in the end, they will interfere with each other (marginal productivity will become negative) and output will decrease.

Marginal productivity of labor(marginal product of labor - MPL) is the increase in output from each subsequent unit of labor i.e. productivity gain to total product (TPL). The marginal product of capital MPK is defined similarly.

The law of diminishing marginal productivity “states that with an increase in the use of any factor of production (while the others remain unchanged), sooner or later a point is reached at which the additional use of a variable factor leads to a decrease in the relative and further absolute volumes of output. An increase in the use of one of the factors (with the rest fixed) leads to a consistent decrease in the return of its application.

The law of diminishing marginal productivity has never been proven strictly theoretically, it is derived experimentally. If we assume that the law will not be fulfilled, then, for example, it is possible, for example, on a limited plot of land, by increasing the amount of fertilizer, to obtain food for the whole world. This, of course, is not realistic.

The law of diminishing returns begins its operation from the second stage of production, when marginal productivity begins to fall. The level from which the decrease in marginal productivity begins depends on the nature of the production function.

29. The choice of production technology. Isoquant. Marginal rate of technological substitution.

Suppose that only 2 resources are used in production, for example, labor (L) and capital (K) (Figure 5.2). If we connect all combinations of resources, the use of which will provide the same amount of output, then we get isoquants.

An isoquant, or constant product curve, is a curve representing an infinite number of combinations of factors of production that provide the same output.

An isoquant lying above and to the right of another represents a larger volume of output. The set of isoquants, each of which shows the maximum output achieved by using certain combinations of resources, is called an isoquant map.

The marginal rate of technical substitution or technological replacement (MRTS) is the amount of one resource that can be reduced in exchange for a unit of another resource while maintaining the same total output.

The slope of the isoquant measures the marginal rate of technological substitution. The marginal rate of technological substitution shows how much capital can be replaced by one additional unit of labor, provided that output remains unchanged.

30. The rule of cost minimization. Isocost. Producer balance.

The cost minimization rule is as follows: the cost of producing a certain volume of output becomes minimal if the ratio of the marginal product of one factor of production to its price is equal to the ratio of the marginal product of another factor of production to its price: MP 1 /P 1 = MP 2 /P 2, where 1 and 2 are factors of production.

Isocost is a set of points in the plane, each of which corresponds to a set of certain volumes of two factors of production (for example, K - capital and L - labor), acquiring which the entrepreneur will spend the same amount of money.

An isocost map is a graph that shows isocosts corresponding to different levels of an entrepreneur's costs of factors of production.

Using the isocost, it is possible to determine which set of factors of production provides a given output with the lowest total cost (TC). The solution to this problem is at the point of contact (ε) of the isocost with the isoquant, which reflects the equilibrium of the producer.

For a given level of costs, all possible combinations of factors of production must lie on the isocost; at the same time, its slope will reflect the ratio of factor prices (P L /P K). All technologically effective combinations of factors will lie on an isoquant, the slope at each point of which expresses the ratio of marginal factor productivity (MP L /MP K). The optimization condition (MP L /MP K = P L /P K) will be satisfied if the slopes of the isocost and isoquant are equal.

Therefore, the optimum will be reached at the point A of contact between the isoquant and the isocost. For the isoquant, this is the point of replacement of factors of production, expressed in terms of the ratio of their marginal products, for the isocost, the point of replacement of factors of production, expressed in terms of the ratio of their prices.

The minimum production costs are achieved under the condition that the ratio of the marginal productivity of production factors is equal to the ratio of their prices. The condition for minimizing production costs is at the same time the condition under which the equilibrium of the producer is reached, since there is no other combination of factors that can ensure greater production efficiency.

31. Production costs and their classification.

To carry out its activities, the firm incurs certain costs associated with the acquisition of the necessary production factors and the sale of manufactured products. The valuation of these costs is the costs of the firm.

Production costs are the costs of production, expressed in terms of value, associated with the rejection of alternative uses of resources. Production costs - the total cost of living and materialized (past) labor for the production of a product, commodity, service in monetary terms

The principle of alternativeness in determining production costs shows that the actual level of costs should be estimated at the current cost of the resource and taking into account lost profits.

Production costs:

Accounting costs - actual costs incurred in cash associated with the implementation of production (only payments and accruals that must be taken into account in accordance with legal acts on accounting.)

Economic costs - the opportunity cost of resources diverted from this production. (Explicit, implicit costs)

The costs are:

external ( explicit) - resources purchased by the firm (accounting costs);

Explicit costs- the amount of payments for acquired factors (wages of hired workers, payments to suppliers of material resources, payments on bank loans, payment for transport, energy, etc.).

internal(implicit, or implicit) - the company's own resources (not reflected in the financial statements).

Implicit costs- this is the cost of services of factors of production that are used in the production process, but are not purchased (for example, belonged to the owner of the firm). Their value is equal to the cash flows that could be obtained under the best alternative use. They are difficult to account for in contracts and are rarely fully valued in cash.

All these costs are usually returnable and are taken into account when making economic decisions along with economic (opportunity) costs.

Return costs are the costs that the firm may not incur by terminating its activities.

Only one category of costs is not taken into account when making important decisions for the firm on the scale of activities - irrevocable. sunk costs associated with previously committed and irrecoverable expenses at the time of closing the company. These include the cost of creating highly specialized equipment, advertising costs, etc.

32. Dynamics of production costs in the short run.

The short run is the period when most of the production remains constant, fixed, and in order to increase (or decrease) the volume of production, the firm can change only one factor of production.

In the long run, the firm can make changes to all factors of production. It can not only hire additional workers, but also build or purchase additional premises and equipment to meet the new market conditions.

In the dynamics of costs in the short term, the following can be distinguished:

- 1. simultaneous reduction of marginal, average variable and total costs;

- 2. decrease in average variables and total averages with an increase in marginal costs;

- 3. increase in marginal and average variables with a decrease in average total costs;

- 4. simultaneous increase in all types of costs.

33. Production costs in the long run.

The long-term production period is the time interval during which the enterprise can change the amount of all employed resources, including the number of production capacities. From an industry point of view, in the long run, there is movement not only within firms to expand or curtail output, but also movement within the industry: some firms leave it, completely curtailing production, and some newly formed ones may come.

In the long run, all factors of production can be changed, and accordingly there will be no division into fixed and variable costs, and only average and marginal costs will be considered. According to its content, long-term production costs reflect changes in costs depending on changes in the scale of production. The nature of these changes will be determined by the type of scale (assuming the prices of factors of production remain unchanged): with a growing scale effect, the average long-term costs will decrease, with a constant one, they will remain unchanged, with a decreasing one, they will increase.

In the long run, the producer can choose any size of production. However, when solving the problem of optimizing production in terms of costs, he must choose such a scale of production at which output would be carried out with the minimum average long-term costs. Under this condition, the optimal size of the enterprise will be such that the equality of long-term average and marginal costs (LMC = LAC) is achieved.

Long run cost curves show the minimum cost of producing any given quantity of output when all factors are variable.

Long-run marginal cost characterizes the increase in costs with an increase in output per unit, if all production resources are variable.

Long-term average costs characterize the unit (average) costs per unit of output, provided that all production resources are variable. The main difference between long-term and short-term analysis is the measure of resource factor elasticity. In the long term, producers have opportunities that are not feasible in the short term. In the long run, the manager can control output and costs by changing not only the intensity of production activity in the enterprise, but also the size and number of enterprises.

34. Income and profit of the firm.

The cash income that the firm receives as a result of the sale of manufactured products takes the form of total (cumulative) income (TR), the value of which depends on the market price (P) of the goods sold and the amount of products sold by the firm (Q), i.e. TR = P *Q.

Income can be analyzed both from the standpoint of changes in its total value, and from the standpoint of assessing the profitability of products, as well as the nature of its changes. For this purpose, the indicators of average and marginal income are used. Average income (AR) - the amount of income per unit of product sold, i.e. AR= TR/Q. Marginal income (MR) - the increase in total income from an additional unit of output sold, i.e. MR=ΔTR/ΔQ.

The firm's profit is formed as the difference between total income and total costs, and its changes are described by the function n(q) = TR(q) - TC(q).

Accounting profit is the difference between total revenue and accounting costs, which are actually payments made for the resources involved in the production of goods.

Economic profit is defined as the difference between total revenue and economic costs.

There are two approaches to profit maximization analysis. One of them is based on comparing the absolute values of income and costs, the other is based on marginal analysis and consists in comparing marginal income and marginal costs.

The comparison of total revenue and total costs is based on the fact that the maximum amount of economic profit will be obtained when an additionally sold unit of production does not give an increase in profit. The amount of profit is the difference between total revenue and total production costs, the values of which are functionally dependent on the produced and sold quantity of products.

The maximum profit is achieved at the volume q 2 , where the difference between the values of total income and total production costs is the largest (BC). At this level of output, the slope of the total cost curve (point C) is equal to the slope of the total income curve (point B).

The firm maximizes profit at the level of output at which total revenue exceeds total cost of production by the greatest amount.

The comparison of marginal revenue and marginal cost is an example of marginal analysis and relies on the comparison of marginal benefits (MR) and marginal cost (MC) as a principle of maximization.

The principle of maximization says that in order to achieve maximum profit, the firm must choose the level of output at which the values of marginal revenue and marginal cost are equal.

35. State regulation of the economy, its forms and methods.

State regulation- a set of measures, actions applied by the state for corrections and the establishment of basic economic processes.

The state is responsible for:

- Fiscal policy (budget, taxes)

- Monetary policy (cash, credit market regulation)

- Regulation of foreign trade

- Regulation of income distribution

Mechanisms of state regulation of market economy:

- Fiscal (fiscal) policy is the activity of the state in the field of taxation, regulation of public spending and the state budget. It is aimed at ensuring the stable development of the economy, preventing inflation and providing employment for the population.

- Monetary (monetary) policy - control over the money supply in the economy. Its goal is to support the stable development of the economy.

Regulation methods are divided into:

- Direct: control over monopolies, ecology, development of standards, their maintenance (quality marks, state standards)

- Indirect: monetary policy, income control, social policy

- Foreign economic regulation

Forms of regulation

- State target programs (social)

- Forecasting

- Situation modeling

State regulation also extends to the technical aspects of activity. This is the so-called "technical regulation". This regulation has common "centralized mechanisms" that are also characteristic of economic regulation: regulation, certification and supervision, licensing, accreditation, delegation, registration, sanctions and appeals.

Reasons for regulation: 1) The presence of public goods in the country (education, health care, environmental protection, etc.) 2) The presence of private and public production 3) The emergence of negative effects within the market (poverty, crime, environmental problems) 4) Scientific and technical progress 5) Tendency towards monopolization 6) Presence of international competition.

36. National economy. National accounting system.

« National economy- this is a system of social reproduction of the country that has historically developed within certain territorial boundaries, an interconnected system of industries and types of production, covering all the established forms of social labor.

The ultimate overall goal of the national economy is to provide conditions for the optimal life of all members of society on the basis of economic growth.

This common goal is integrated from a number of more specific goals:

Stable high growth rates of national output

Efficient production

Stability

High Employment Rate, Efficient Employment

Maintenance of foreign trade balance achievement of social justice in the division of society's income.

The basis of the national economy is enterprises, firms, organizations, households, united into a single system by economic relations, performing certain functions in the social division of labor, producing goods and services.

The national economy consists of two major areas: the production of goods (material production) and the provision of services.

System of National Accounts is a balance of interrelated indicators characterizing the production, distribution, redistribution and final use of the final product and national income. At the heart of building a system of national accounting (SNA) is the concept of "economic circulation", the core of which is the economic turnover.

37. Main macroeconomic indicators. Definition of GDP, ways to measure it.

Main macroeconomic indicators:

GDP (gross domestic product) - measures the value of the final product produced in the territory of a given country for a certain period, regardless of whether the factors of production are owned by citizens of this country or owned by foreigners.

GNP (gross national product) - reflects the ownership of the produced product of the nation and differs from GDP by the amount of net factor income from abroad (YF):

GNP=GDP + YF.

Three main methods are used to calculate GDP:

The Law of Diminishing Marginal Productivity is one of the generally accepted economic statements, according to which the application of one new factor of production leads to a decrease in output over time. Most often, this factor is optional, that is, not mandatory in a particular industry. It can be applied intentionally, directly in order to reduce the number of goods produced, or due to a combination of certain circumstances.

What is the theory of diminishing productivity based on?

As a rule, the law of diminishing marginal productivity plays a key role in the theoretical part of production. It is often compared to the waning proposition that occurs in consumer theory. The comparison lies in the fact that the sentence mentioned above tells us how much each individual buyer, and the consumer market in principle, maximizes the goods produced, and also determines the nature of the demand for pricing policy. The law of diminishing marginal productivity affects precisely the steps taken by the manufacturer, the maximization of profits and the dependence of the set price on demand from his side. And in order to make all these complex economic aspects and issues clearer and more transparent for you, we will consider them in more detail and with specific examples.

Pitfalls in the economy

To begin with, let's define the very meaning of the wording of this statement. The law of diminishing marginal productivity is by no means a decrease in the quantity of goods produced in one way or another over the course of all centuries, as it appears on the pages of history textbooks. Its essence lies in the fact that it works only in the case of an invariable, if something is intentionally “inscribed” in the activity that slows down everyone and everything. Of course, this law does not apply in any way when it comes to changing performance features, introducing new technologies, and so on and so forth. In this case, you say, it turns out that the small enterprise has more than its larger counterpart, and this is the essence of the whole question?

Reading the words carefully...

In this case, we are talking about the fact that productivity is reduced due to variable costs (material or labor), which, accordingly, are larger in a large enterprise. The law of diminishing marginal productivity is triggered when this very marginal productivity of a variable factor reaches its maximum in terms of costs. That is why this formulation has nothing to do with increasing the production base in any industry, no matter what it is characterized by. In this matter, we only note that not always an increase in the volume of produced commodity units leads to an improvement in the state of the enterprise and the whole business as a whole. It all depends on the type of activity, because each individual species has its own optimal limit for the growth of production. And if this limit is exceeded, the efficiency of the enterprise, respectively, will begin to decline.

An example of how this complex theory works

So, in order to understand exactly how the law of diminishing marginal productivity works, let's consider it with a clear example. Suppose you are the manager of a certain enterprise. A production base is located on a specially designated area, where all the equipment necessary for the normal functioning of your company is located. And now it's up to you to produce more or less goods. To do this, you need to hire a certain number of workers, draw up an appropriate daily routine, and purchase the right amount of raw materials. The more employees you have, the tighter your schedule, the more foundation you will need for your product. Accordingly, production volumes will increase. It is on this that the law of diminishing marginal productivity of factors that affect the quantity and quality of work is based.

How does this affect the selling price of the product?

We go further and take into consideration the question of Of course, the owner is a gentleman, and he himself has the right to set the desired fee for his goods. However, focusing on market indicators that have long been established by your competitors and predecessors in this field of activity is still worth it. The latter, in turn, tends to constantly change, and sometimes the temptation to sell a certain batch of goods, even if “under-released”, becomes great when the price reaches its maximum on all exchanges. In such cases, in order to sell as many items as possible, one of two options is chosen: increasing the production base, that is, raw materials and the area on which your equipment is located, or hiring more employees, working in several shifts, and so on. Further. This is where the law of diminishing marginal productivity of returns comes into play, according to which each subsequent unit of the variable factor brings a smaller increment in total production than each previous one.

Features of the decay formula

Many, after reading all this, will think that this theory is nothing but a paradox. In fact, it occupies one of the fundamental positions in the economy, and it is based not at all on theoretical calculations, but on empirical ones. The law of diminishing labor productivity is a relative formula derived through many years of observation and analysis of activities in various areas of production. Delving into the history of this term, we note that for the first time it was voiced by a French financial expert named Turgot, who - as a practice of his activity - considered the features of the work of agriculture. Thus, for the first time, the "law of diminishing soil fertility" was introduced in the 17th century. He said that a constant increase in labor applied to a certain plot of land leads to a decrease in the fertility of this plot.

A bit of Turgot's economic theory

Based on the materials that Turgot presented in his observations, the law of diminishing productivity of labor can be formulated as follows: "The assumption that increased costs will give in the future an increased volume of product is always false." Initially, this theory had a purely agricultural background. Economists and analysts argued that on a plot of land, the parameters of which do not exceed 1 hectare, it is impossible to grow more and more crops in order to feed many people with them. Even now, in many textbooks, in order to explain to students the law of diminishing marginal productivity of resources, it is the agricultural industry that is used as a clear and most understandable example.

How it works in agriculture

Let's now try to understand the depth of this question, which is based on a seemingly banal example. We take a certain plot of land on which more and more centners of wheat can be grown every year. Up to a certain point, each addition of additional seeds will bring an increase in production. But there comes a turning point when the law of diminishing productivity of the variable factor comes into force, which implies that the additional costs of labor, fertilizers and other parts needed in production begin to exceed the former level of income. If you continue to increase production on the same plot of land, then the decrease in former profits will gradually turn into a loss.

But what about the competitive factor?

If we assume that this economic theory has no right to exist in principle, we get the following paradox. Let's say growing more and more spikelets of wheat on one plot of land will not be so expensive for the producer. It will be spent on each new unit of its production in the same way as on the previous one, while constantly only increasing the volume of its goods. Consequently, he will be able to perform such actions indefinitely, while the quality of his products will remain the same high, and the owner will not have to purchase new territories for further development. Based on this, we get that the entire amount of wheat produced can be concentrated on a tiny plot of soil. In this case, such an aspect of the economy as competition simply excludes itself.

We form a logical chain

Agree that this theory has no logical basis, since everyone has known since time immemorial that any wheat present on the market differs in price depending on the fertility of the soil on which it was grown. And now we come to the main thing - it is the law of diminishing returns of productivity that explains the fact that someone cultivates and uses more fertile soil in agriculture, while others are content with soils of lower quality and suitable for such activities. Indeed, otherwise, if every additional centner, kilogram or even gram could be grown on the same fertile plot of land, then no one would have come up with the idea of cultivating land less suitable for agricultural industry.

Features of former economic doctrines

It is important to know that in the 19th century, economists still fit this theory exclusively into the field of agriculture, and did not even try to take it out of this framework. All this was explained by the fact that it was in this industry that such a law had the greatest amount of obvious evidence. Among these, one can name a limited production zone (this is a land plot), a rather low pace of all types of work (processing was carried out manually, wheat also grew naturally), in addition, the range of crops that can be grown was quite stable. But given the fact that scientific and technological progress has gradually covered all areas of our lives, this theory quickly spread to all other areas of production.

On the way to modern economic dogmas

In the 20th century, the law of diminishing productivity finally and irrevocably became universal and applicable to all types of activity. The costs that were used to increase the resource base could increase, but without territorial increase, further development simply could not be. The only thing that manufacturers could do without expanding their own boundaries of activity was to purchase more efficient equipment. Everything else - an increase in the number of employees, work shifts, etc. - inevitably led to an increase in production costs, and incomes grew at a much lower percentage compared to the previous indicator.

24. Factors of production of the firm. The production function of the firm. The law of diminishing productivity of factors of production.

Production is the basis of the business activity of the company. After all, income is a realized product or service. Commercial activity is preceded by industrial activity.

Production is the process of creating goods necessary for consumers: material and intangible goods (services). In this case, firms use factors of production, which are also called input (input) production factors.

The factors of production used by the firm are divided into constants and variables. Fixed factors of production are those whose quantity remains unchanged during the production of a given product (for example, machine tools in the production of a given batch of shoes). Variable factors of production - those factors, the amount of which changes during the production of a given product (for example, electricity, raw materials).

For example, the owner of a candy store uses such inputs as the labor of confectioners and sales assistants, raw materials in the form of flour, sugar, yeast, as well as capital represented by mixers, ovens, baking dishes, etc.

The factors of production are usually divided into three main categories: labor, capital, materials.

Labor as a production factor includes skilled and unskilled labor, as well as entrepreneurial activity.

The relationship between the input factors and the final product output is described production function. It is the starting point in the microeconomic calculations of the company, allows you to find the best option for using production capabilities.

Law of diminishing marginal productivity

Suppose that F 1 is a variable factor, while the other factors are constant:

Total product (Q) is the amount of an economic good produced using some amount of a variable factor. Dividing the total product by the amount of the variable factor consumed, we obtain average product (AR).

Marginal Product (MP) is defined as the increase in total product resulting from infinitesimal increments in the amount of variable factor used:

Factor substitution rule: the ratio of the increments of the two factors is inversely related to the magnitude of their marginal products.

Law of diminishing marginal productivity States that With an increase in the use of any factor of production (while the rest remain unchanged), sooner or later a point is reached at which the additional use of a variable factor leads to a decrease in the relative and further absolute volumes of output.

The resource use rule can be expressed as MRP = MRC, where MRP is the marginal product in monetary terms and MRC is the marginal cost.

25. Production grid and isoquant. Isocost.

Q = f(K, L), where To- capital, L- labor.

Production grid (Q=F(L,K))

|

Capital cost (K) |

Labor cost (L) |

|||||

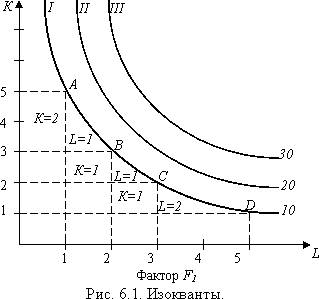

The production grid shows that the same amount of output can be produced with different combinations of factors of production. For example, Q=85 units can be produced with a combination of factors 200K and 30L and with a combination of 100K and 60L.

If we connect all combinations of resources, the use of which provides the same amount of output, we get isoquants.

Isoquanta is a curve that reflects the various combinations of resources that can be used to produce the same amount of output.

Isoquants for the production process mean the same as indifference curves for the consumption process. They have similar properties: 1. have a negative slope, 2. are convex relative to the origin, 3. do not intersect with each other, 4. isoquant, lying above and to the right of the other, represents a larger volume of output, 5. show real levels of production: 10 thousand, 20 thousand, 30 thousand, etc.

The concave shape of the isoquant shows that the marginal rate of technological substitution decreases as one moves down the isoquant. This means that labor and capital are not absolutely interchangeable, and therefore there are certain difficulties in replacing capital with labor, i.e. there are certain limits of interchangeability of factors.

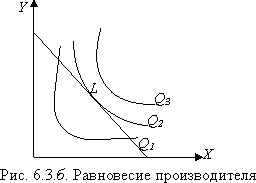

The amount of money that the company has to organize production is called the budget constraint (graphically - a straight line, isocost).

Isocost - a straight line showing all combinations of resources, the use of which requires the same cost.

, where - Р To and R L - respectively, the price of a unit of capital and a unit of labor

Using the same method as in determining the equilibrium of the consumer, we combine the isocost map with the isocost and the touch point will show the largest volume of production for given budget possibilities (Figure 6.3 .b.).

Using the same method as in determining the equilibrium of the consumer, we combine the isocost map with the isocost and the touch point will show the largest volume of production for given budget possibilities (Figure 6.3 .b.).

Producer equilibrium- the state of the producer in the process of replacing one factor of production with another, when the last ruble spent on each resource brings the same marginal product.

Mathematically, the system of equilibria is described by a system of equations. ![]() - a condition for optimizing production - choosing from all possible options for using resources those that give the best option. In order to see the prospects for the development of an enterprise in the long term, it is necessary to imagine how the volume of production and the cost of acquiring factors will increase at each stage of the growth in production volume. Let's connect isoquants with isocosts by points of contact, we will get the trajectory of the economic activity of the company or the production activity of the enterprise isoclinal line OK (Fig. 6.3. in)

- a condition for optimizing production - choosing from all possible options for using resources those that give the best option. In order to see the prospects for the development of an enterprise in the long term, it is necessary to imagine how the volume of production and the cost of acquiring factors will increase at each stage of the growth in production volume. Let's connect isoquants with isocosts by points of contact, we will get the trajectory of the economic activity of the company or the production activity of the enterprise isoclinal line OK (Fig. 6.3. in)

| " |

1. The essence of the law. With an increase in the use of factors, the total volume of production increases. However, if a number of factors are fully involved and only one variable factor increases against their background, then sooner or later there comes a moment when, despite the increase in the variable factor, the total volume of production not only does not grow, but even decreases.

The law says: an increase in the variable factor with fixed values of the rest and the invariance of technology ultimately leads to a decrease in its productivity.

2. Operation of the law. The law of diminishing marginal productivity, like other laws, operates in the form of a general trend and manifests itself only when the technology used is unchanged and in a short period of time.

In order to illustrate the operation of the law of diminishing marginal productivity, one should introduce the concepts:

- common product- the production of a product using a number of factors, one of which is variable, and the rest are constant;

- average product- the result of dividing the total product by the value of the variable factor;

- marginal product- increment of the total product due to the increment of the variable factor.

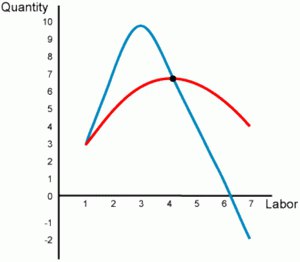

If the variable factor is incremented continuously by infinitesimal values, then its productivity will be expressed in the dynamics of the marginal product, and we will be able to track it on the graph (Fig. 15.1).

Rice. 15.1.Operation of the law of diminishing marginal productivity

Let's build a graph where the main line OAHSV– dynamics of the total product:

1. Divide the curve of the total product into several sections - cuts: OB, BC, CD.

2. On the segment OB, we arbitrarily take point A, at which the total product (OM) equal to variable factor (OR).

3. Connect the dots O and BUT- we will get the RAR, the angle of which from the point of coordinates of the graph will be denoted?. Attitude AR to OR– the average product, also known as tg ?.

4. Draw a tangent to point A. It will intersect the axis of the variable factor at point N. A APN will be formed, where NP- marginal product, also known as tg ?.

On the whole segment OV tg? the law of diminishing marginal productivity does not show its effect.

On the segment sun the growth of the marginal product is reduced against the background of the continuing growth of the average product. At the point FROM marginal and average product are equal to each other and both are equal?. Thus began to appear law of diminishing marginal productivity.

On the segment CD the average and marginal products are declining, and the marginal product is faster than the average. At the same time, the total product continues to grow. Here the operation of the law is fully manifested.

Behind the dot D, despite the growth of the variable factor, an absolute reduction even of the total product begins. It is difficult to find an entrepreneur who would not feel the effect of the law beyond this point.

In the short run, when one factor of production remains unchanged. The operation of the law assumes an unchanged state of technology and production technology. If the latest inventions and other technical improvements are applied in the production process, then an increase in the volume of output can be achieved using the same production factors, i.e., technological progress can change the boundaries of the law.

If capital is a fixed factor and labor is a variable factor, then the firm can increase production by employing more labor. But according to the law of diminishing marginal productivity, a consistent increase in a variable resource, while the others remain unchanged, leads to diminishing returns of this factor, i.e., to a decrease in the marginal product or marginal productivity of labor. If the hiring of workers continues, then in the end, they will interfere with each other (marginal productivity will become negative), and output will decrease.

The marginal productivity of labor (the marginal product of labor - $MP_L$) is the increase in the volume of production from each subsequent unit of labor:

$MP_L=\frac (\triangle Q_L)(\triangle L)$,

those. productivity gain to total product ($TP_L$) is equal to

$MP_L=\frac (\triangle TP_L)(\triangle L)$

The marginal product of capital $MP_K$ is defined similarly.

Based on the law of diminishing productivity, let's analyze the relationship between the total ($TP_L$), average ($AP_L$) and marginal products ($MP_L$), (Fig. 1).

There are three stages in the movement of the total product curve ($TP$). At stage 1, it rises at an accelerating pace, since the marginal product ($MP$) increases (each new worker brings more production than the previous one) and reaches a maximum at point $A$, i.e., the growth rate of the function is maximum. After point $A$ (stage 2), due to the law of diminishing returns, the $MP$ curve falls, i.e. each hired worker gives a smaller increment of the total product compared to the previous one, so the growth rate of $TP$ after $TC$ slows down . But as long as $MP$ is positive, $TP$ will still increase and reach its maximum at $MP=0$.

Figure 1. Dynamics and relationship of total, average and marginal products

At stage 3, when the number of workers becomes excessive in relation to fixed capital (machines), $MP$ becomes negative, so $TP$ starts to decrease.

The configuration of the average product curve $AP$ is also determined by the dynamics of the curve $MP$. At stage 1, both curves grow until the increment in output from newly hired workers is greater than the average productivity ($AP_L$) of previously hired workers. But after the point $A$ ($max MP$), when the fourth worker adds less to the total product ($TP$) than the third, $MP$ decreases, so the average output of four workers also decreases.

scale effect

Manifested in the change in long-term average production costs ($LATC$).

The $LATC$ curve is the envelope of the firm's minimum short-term average cost per unit of output (Fig. 2).

The long-term period in the company's activity is characterized by a change in the number of all production factors used.

Figure 2. Curve of long-term and average costs of the firm

The reaction of $LATC$ to a change in the parameters (scale) of a firm can be different (Fig. 3).

Figure 3. Dynamics of long-term average costs

Figure 4

Suppose that $F_1$ is a variable factor, while the other factors are constant:

total product($Q$) is the amount of an economic good produced using some amount of a variable factor. Dividing the total product by the amount of the variable factor consumed, we obtain the average product ($AP$).

Marginal product ($MP$) is defined as the increase in total product resulting from infinitesimal increments in the amount of variable factor used:

$MP=\frac (\triangle Q)(\triangle F_1)$

Factor substitution rule: the ratio of increments of two factors is inversely related to the value of their marginal products.

Law of diminishing marginal productivity argues that with an increase in the use of any production factor (while the others remain unchanged), sooner or later a point is reached at which the additional use of a variable factor leads to a decrease in the relative and then absolute volumes of output.

Remark 1

The law of diminishing productivity has never been proven strictly theoretically, it is derived experimentally.

Factors of production are used in production only when their productivity is a positive value. If we denote the marginal product in monetary terms as $MRP$, and the marginal cost as $MRC$, then the resource use rule can be expressed by equality.