Ways to increase the profits of trade organizations. How to increase profit

The increase in revenue at the enterprise, according to many experts, is not the main indicator of effective work. It is necessary to evaluate the sales criteria in a comprehensive manner, taking into account the resources used and other costs for the products produced. The increase in the profit of the enterprise, as the main indicator of the success of production, is important.

The main ways, methods, factors to increase the profits of the enterprise

Profit from sales is the value that is obtained as the difference between the revenue received and the cost of the product (resources spent and labor costs for its production).

Thus, there are two ways to increase profits:

- increase in the cost of production;

- increase in revenue due to more sales, due to cost reduction.

Reducing the cost, in addition to increasing profits, leads to an increase in the competitiveness of the goods produced.

Factors that affect the reduction in unit production costs:

- increasing the productivity of labor processes;

- provision of production with working capital;

- taking measures to optimize time and fixed costs for the production of goods;

- reduction of expenses for economic activity;

- carrying out activities to optimize the management of the enterprise.

To increase the number of sales (increase in the volume of goods sold), it is necessary: to have flexible technological processes that can quickly reconfigure to release a new product, to improve the quality of products of existing products.

In addition, it is important to conduct marketing activities, conclude new contracts for the sale of goods. In order to understand which of the ways of development of the enterprise affects the profit in a particular case, an analysis of the change in the profit received is carried out.

Analysis of changes in enterprise profit

When analyzing the change in profit in production, the reasons for the fall in this indicator are first determined, and additional reserves are searched for at the enterprise. It also explores what management decisions can affect profits.

AT analysis process:

- the effectiveness of financial activity is assessed, how the implementation of planned production tasks is carried out;

- it is considered what the profit of the enterprise is obtained from, its structure and components;

- the factors influencing the receipt and formation of profit are determined;

- it is established how profit is distributed in production, an estimate of proportional distribution is given;

- reserves are identified and counted.

There is a general methodology for determining the necessary parameters for making a profit. Reporting financial documentation is used during this process. Thus, the structure of profit is determined (everything that is included in the cost of production), the study of sales volumes, the calculation of the profitability of the company's assets, and the determination of net profit.

An important point in the analysis is to find out the factor influencing the growth or decline of profits.

Directions and measures to increase the profit of the enterprise

Since the profit of an enterprise is the final indicator of its economic activity, measures to ensure a stable indicator of profit and its growth are always important - this is called profit planning.

The profit of the enterprise must be planned in order to:

- shareholders and owners could see dividends, and what investments are invested in the enterprise, how the distribution of the enterprise's funds is carried out (modernization of equipment, increase in payments for labor);

- efficient use of funds;

- determine production reserves.

There are three methods by which profit is planned:

- direct calculation when production has a small assortment of products;

- the method of interconnection of costs and revenues, "Direct-Costing";

- an analytical method of profit planning, often used with a large assortment of manufactured goods.

Calculations of projected profit are the basic parameters for investors, partners (suppliers of raw materials).

Increasing the profit of a trading enterprise at the expense of costs

To make a profit, a trading company conducts various activities, market research by marketers, business organization, but few people understand that by reducing costs, you can significantly increase profits.

Experts have developed ways, adhering to which you can reduce costs in the enterprise, these are:

- lowering the cost of goods by reducing costs in the production, economic, general production sectors;

- drawing up a list of measures to eliminate problems with responsible persons and deadlines;

- reduction of costs for specific items of cost items, according to the analysis.

To reduce costs for greater profits, a systematic approach is important, which includes:

- organizational accounting and strict reporting. The top manager of the enterprise, the head are responsible for this;

- analytical measures to identify irrecoverable losses from economic activity (losses in working time, defective products);

- improvement of control and checks is a good incentive to raise discipline, identify shortages;

- conducting comprehensive audits of the enterprise, during which unaccounted expenses are clarified, plans are drawn up to reduce the identified losses.

To increase profits, the management of the enterprise must constantly be in search of new ways to reduce costs. But all actions should go to the benefit of production, and not to the detriment.

Reserves for increasing profits and profitability of the enterprise

The production capacity of the enterprise, which increases with an increase in sales, is called a reserve for increasing profits. When planning further activities, reserves are simultaneously determined that can be used.

Then, engineering, economic, social measures are developed to attract these reserves. In the course of this work, constant monitoring is important, since the implementation of the plan takes a certain period of time and is unusually not one-time.

An important share in the search for reserves is cost savings:

- in the amount of energy consumed (you can introduce energy-saving technologies);

- in volumes of materials and fuel;

- in the cost of rent (sometimes the option of buying out production facilities or transferring production to another cheaper building is considered).

The calculation of reserves in production is carried out by the comparison method. Therefore, it is important to determine the existing indicators of the enterprise. For comparison, the planned level of resources is used, taking into account established standards and the achievements of advanced enterprises, as well as the average value for the industry.

Enterprises expand customer base at Expocentre exhibitions

Exhibitions The Central Exhibition Complex "Expocentre" is famous all over the world. Industry exhibitions are visited by entrepreneurs from different countries. Modern pavilions and conference halls create a comfortable atmosphere for communication between businessmen and discussion (presentation) of new products.

It is live communication at the exhibition that allows you to significantly increase the partner base in business, find new customers for your own products.

Profit - the most important category of the market economy. The identification of factors affecting profit implies the study of the economic conditions for its formation. Economic conditions may be both internal and external. Under their influence, the absolute value and the relative level of profit change. to external conditions include such as: inflation, changes in laws and regulations in the field of pricing, lending, taxation of enterprises, remuneration of employees, etc. To internal conditions, affecting the amount of profit, for example, can be attributed to the number of employees in the enterprise, reducing the number of which, you can thereby increase or decrease the cost of wages, which in turn can affect the amount of gross profit and, accordingly, the amount of net profit. Factors, affecting the amount of profit can be divided into two groups. The first group includes the so-called main factors that directly affect the amount of profit of the enterprise. . The main ways to increase profits. Each enterprise should provide for planned measures to increase profits. In general, these measures can be of the following nature: increasing output improving product quality selling or leasing surplus equipment and other property reducing production costs through more rational use of material resources, production capacities and areas, labor force and working hours diversification of production expansion of the sales market and more.

16. Profitability: the essence and meaning of the category. Types of profitability, methods of their calculation.

The total amount of profit received by the enterprise cannot fully characterize the effectiveness of its production and economic activities, since its value is determined by the size of the enterprise. Therefore, there is a need for a relative characteristic of the profitability (profitability) of the enterprise in the form of a comparison of the profit received with the amount of fixed and working capital. This ratio, expressed as a percentage, characterizes the profitability, i.e. degree of profitability. According to profitability indicators, it is possible to compare the efficiency of enterprises. In accordance with the types of profit, the following profitability indicators are distinguished: overall profitability; enterprise profitability; return on equity; profitability of certain types and products in general; profitability of sales. Overall profitability Rtot is defined as the ratio of the balance sheet profit Pb to the average annual cost of the fixed production capital FSG and the normalized working capital Phos,%: Rtotal \u003d Pb * 100 / (Fsg + Phos). The overall profitability characterizes the size of the total profit received per ruble of invested funds. If an enterprise, with a constant value of production capital, will use it better, it will receive a greater economic effect, which will cause an increase in profitability. However, the rate of return is important for the enterprise, which it can use for its own needs, since the enterprise transfers part of the profit to the budget in the form of real estate taxes, income tax and transport fees. If it is less than the bank interest on deposits, then the company will not be profitable to engage in this business.

Therefore, it is very important to calculate the profitability of the net profit remaining at the disposal of the enterprise, i.e. enterprise profitability. Profitability of the enterprise(Rnp) is defined as the ratio of Pch's net profit to the average annual cost of the main production and normalized working capital,%: Rpr \u003d Pch * 100 / (Fsg + Phos) According to this indicator, the results of the enterprise are evaluated. Return on equity is determined by the ratio of net profit to the value of equity Kc: Rsk \u003d Pch * 100 / Ks. Profitability of individual types and products in general is determined by the ratio of profit from the sale of products (Pr) to its total cost (Cp),%: Rprod \u003d Pr * 100 / Sp. This indicator reflects the cost effectiveness of living and materialized labor. It is mainly used for planning and accounting for the profitability of the production of certain types of products. Return on sales (turnover) ( Rob) is calculated by the ratio of profit from the sale of products /

Profit is formed under the influence of a large number of interrelated factors that affect the performance of the enterprise in different directions: some positively, others negatively. Moreover, the negative impact of some factors can reduce or even negate the positive impact of others. The variety of factors does not allow them to be clearly limited, and causes their grouping. Considering that an enterprise is both a subject and an object of economic relations, the most important is their division into external and internal.

Among external factors, the following can be distinguished: economic conditions of management, market capacity, effective demand of consumers, state regulation of the activities of trade enterprises, etc. The level, dynamics and fluctuation of effective demand is of particular importance, because it predetermines the stability of obtaining trade revenue.

The next significant factor is the prices set by the suppliers of goods. In a competitive environment, an increase in purchase prices is not always accompanied by an adequate increase in sales prices. Retailers often compensate for part of the increase in prices by suppliers by reducing the share of their own profits in the retail price of goods. An increase in prices for the services of transport enterprises, utilities and other similar enterprises directly increases the current costs of a trading enterprise, thereby reducing profits.

Profit performs three main functions. Profit, first of all, is used as an indicator for evaluating the results of an independent activity of an enterprise, since it reflects all aspects of its activity, both in the sphere of production and in the sphere of circulation. However, profit is not a universal indicator of the enterprise's performance, since its value is largely determined by factors independent of the activity of this enterprise (price policy, changes in turnover tax rates, structural shifts, etc.). The multifactor nature of the economic category of profit makes it necessary to use other indicators of production efficiency along with profit (sold products, labor productivity, turnover rate of working capital, etc.).

The second profit function is distribution. Profit is used as a means of distributing the surplus product and its monetary form - net income between the enterprise and society represented by the state, between the enterprise and the industry, between the enterprise and its employees, between the sphere of material production, where the surplus product is created, and the non-productive sphere, which contains society through surplus

with the process of economic stimulation of the enterprise and its employees. Profit is used as a source and condition for the formation of incentive funds for enterprises and as a major financial resource for expanded reproduction based on technical progress.

The normative profit included in the price and called planned accumulation is the minimum amount of profit: necessary for the successful implementation of self-supporting activities.

The planned profit from execution is closely related to the value of the planned cost. It is formed as the difference between the estimated cost and the planned cost.

Surplus profit is formed when a profit is received in an amount exceeding the planned one.

Unrealized profit accumulates in work in progress, which is reflected in the balance sheet of the contractor until payment, i.e. transformation of work in progress with the object of implementation.

Actual profit is the result of actual costs (actual cost) and is defined as the difference between estimated cost and actual cost.

From the profit (minus the amounts that have a special purpose) priority payments are provided - payment for production assets, fixed payments, interest on a bank loan. Excessive profit also excludes amounts allocated for the repayment of bank loans received to temporarily replenish the lack of own working capital.

The balance sheet profit, reduced by the amount of priority payments, forms the estimated (net) profit, or profit for distribution. From it, deductions are made to economic incentive funds (material incentive fund, fund for socio-cultural measures of housing construction, production development fund). Then part of the profit is directed to cover the planned costs provided for by the financial plan, to centralized capital investments, to repay bank loans granted for capital investments, to increase own working capital, to cover losses in housing and communal services, to reimburse expenses for the economic maintenance of cultural and community institutions .

The main ways to increase profits:

1 Increasing product sales - by increasing the volume of work implemented in the form of technologically completed stages or objects. This is an extensive way to increase profits or profitability;

2 Improve service quality, product quality control - by improving the quality indicators of production: the growth of labor productivity, reducing the material intensity of production, reducing the time and other indicators that ultimately contribute to reducing the cost of work. This is an intense growth path.

3 Sale of surplus equipment or rental - an enterprise sells unnecessary equipment or leases it for a certain period for a certain fee to obtain additional profit.

4 Determining the selling price - the best event to get additional profit.

5 Supplier portfolio diversification

6 Sales market expansion - by expanding the sales territories in the market, profits increase.

7 Hiring More Skilled Workers - due to this, the products become of the highest quality, the products are carried out just in time, etc.

Consider an increase in sales of products:

The assessment of the implementation of the plan for the sale of products for the reporting year is carried out according to the following data:

Table 22 - Analysis of the implementation of the plan for the sale of products for 2009

The table shows that for the reporting year the implementation plan was overfulfilled - by 4.9%. This indicates a decrease in the balance of unsold products.

The analysis of sales of products is closely related to the analysis of the implementation of the plan for the supply of products. Failure to fulfill the plan under contracts for the enterprise turns into a decrease in revenue, profit, and the payment of penalties. In addition, the company may lose markets for products, which will lead to a decline in production. The fulfillment of contracts for the supply of goods for state needs is of particular importance for the enterprise. This guarantees the company the sale of products, timely payment, tax benefits, loans, etc. In the process of analysis, the fulfillment of the supply plan for the month is determined on a cumulative basis for the whole enterprise, in the context of individual consumers and types of products, the reasons for the failure to fulfill the plan are clarified, and an assessment is made of activities to fulfill contractual obligations.

Table 23 - Analysis of the fulfillment of contractual obligations for shipment for March 2009

We calculate the percentage of fulfillment of contractual obligations by dividing the difference between the planned volume of shipment under the contract (OP pl) and its shortfall (OP n) by the planned volume (OP pl):

To d.p. \u003d (OP pl - OP n): OP pl \u003d (10200 - 500): 10200 \u003d 0.95 or 95%.

Short delivery of products negatively affects not only the results of the enterprise, but also the work of trade organizations, allied enterprises, transport organizations, etc.

Having considered the implementation of the plan for the sale of products and the implementation of supply contracts, it is necessary to establish the factors for changing its volume:

Since the company's revenue is determined after payment for the shipped products, the balance of goods can be written as follows:

GP n + TP \u003d RP + GP k., from here

RP \u003d GP n + TP + FROM n - FROM to - GP

Where GP n, GP k - respectively, the balances of finished products in warehouses at the beginning and end of the period;

TP - the cost of output of marketable products;

RP - the volume of sales of products for the reporting period;

FROM n, FROM to - the balance of shipped products at the beginning and end of the month.

The calculation of the influence of these factors on the volume of sales is made by comparing the actual levels of factor indicators with the planned ones and calculating the absolute and relative increments of each of them.

Table 24 - Analysis of the factors of change in the volume of sales of products for 2009

RP = 4800 + 328100 + 3500 - 2300 - 9300 = 324800

The table shows that the plan for sales of products was overfulfilled due to an increase in its output and excess balances of goods shipped to customers at the beginning of the year, a decrease in the balance of finished products at the end of the year. A negative impact on the volume of sales was made by the growth in the balance of shipped products at the end of the year, payment for which has not yet been received on the company's settlement account. Therefore, it is necessary to find out the reasons for the formation of excess balances in warehouses, late payment for products by customers and develop specific measures to accelerate the sale of products and receive revenue.

The growth and development of a trade enterprise is associated with the development and implementation of strategies and tactics for increasing the profitability of an enterprise, through the effective management of the formation and distribution of its income. What is a complex process based on a deep knowledge of market conditions, enterprise capabilities, conditions and factors that determine the competitiveness of an enterprise, the ability to foresee real ways to obtain high performance results.

The profitability of the enterprise is considered not only as the main goal, but also as the main condition for the business activity of the enterprise, as a result of its activities, the effective implementation of its functions to provide consumers with the necessary goods in accordance with the existing demand for them.

In its most general form, profitability characterizes the ratio of the result obtained to the costs that caused this result.

In economic theory, several definitions of the category of profitability are used:

- 1) profitability;

- 2) the ratio of the useful result of trading activity in the form of profit to the cost of the total costs of its receipt;

- 3) comparison of the results of economic activities with costs or resources calculated in value terms;

- 4) an integral indicator summarizing other performance indicators.

In any case, the definition of profitability characterizes the percentage ratio of the amount of profit received to one of the indicators of trade activity.

Currently, in Russian practice, the most common indicator for evaluating the effectiveness of a trading enterprise is the level of profitability of sales (turnover).

Along with indicators of turnover, fixed and working capital, distribution costs, other indicators are also used to calculate the level of profitability, for example, trading space, etc.

Each of the above indicators characterizes the effectiveness of the use of certain types of resources or current costs, but only in aggregate they give an idea of the effectiveness of the trade and economic activities of a trade enterprise as a whole.

In the modern conditions of the functioning of trade enterprises, new opportunities have appeared to increase their profitability, opened up in the course of market transformations, in addition to traditional ones (increase in turnover, reduction in distribution costs, etc.). Among them, the main ones are:

- ? formation of a trade assortment taking into account the profitability of goods;

- ? use of opportunities for risky activities;

- ? innovation policy;

- ? corporatization;

- ? favorable allocation of financial resources and others.

When forming the assortment of goods sold, a trading enterprise should ensure its sufficient breadth and depth, since the more diverse the assortment, the more fully the demand of the population will be satisfied, that is, the buyer is interested in the possibility of a wide choice of goods. And at the same time, it is necessary to ensure the profitability of each commercial transaction: it is advisable to ensure a balanced approach when choosing suppliers, determining the optimal batch and purchase price of goods, establishing a reasonable trade margin, and spending money on commercial activities.

Diversification of the assortment by including interchangeable goods in the assortment list will increase the completeness of purchases, which means it will increase the turnover of the enterprise.

In particular, new customers can be attracted by a more perfect display of goods than other enterprises, thoughtful advertising and promotion, high reputation and specialization of the trading company, additional trading services, lower prices (with the same product quality), ease of purchase (no queues , a wide range of goods), offering goods to buyers, taking into account their buying habits.

An increase in the volume of products sold as a result of a decrease in prices and the cost of trade services is possible with a real decrease in the cost of products intended for sale, an acceleration in the turnover of trade stocks, an increase in inventory and procurement management, the elimination of slow-moving goods, the widespread introduction of self-service, and an increase in the efficiency of the use of retail space.

To increase the profitability of the enterprise, it is necessary to constantly take care of the preservation of available financial resources and their increase. Since market relations imply that money should make money, the owners of temporarily free funds have a problem of how to rationally dispose of them in order to ensure their corresponding growth. This is especially true for a situation with a high level of inflation. Temporarily free funds can be placed on deposits, find an opportunity to interact with financial companies, convert into hard currency, buy bank bills, securities.

To increase profitability, enterprises should take the following measures:

- ? develop and implement new ideas to attract customers to the store: hold exhibitions and sales; organize consultations of specialists in the store; extend store trading hours on weekends and holidays;

- ? improve the skills of employees, which will be accompanied by an increase in their productivity; build an effective system of material incentives for personnel; constantly improve the culture of service, ensure the completeness of the product range;

- ? widely use the means of in-store advertising and information to increase the awareness of customers about the products offered to promote the formation of new areas of demand and save time on the purchase of goods, hold exhibitions, demonstrations, exhibitions and sales;

- ? constantly analyze the state of affairs of competitors, identify its strengths and weaknesses, use experience;

- ? reduction in the level of distribution costs (that is, their size in the price of each product) can be ensured by increasing the volume of sales of goods, the implementation of internal reserves for their savings and other areas of economic activity;

The financial stability of the company, competitiveness, investment attractiveness is affected by net profit. This is the result of the enterprise, formed after the deduction of all costs and taxes. During the crisis years, many enterprises faced a decline in income and sales. To overcome this situation and stay afloat, the company must use ways to increase profits.

Let's look at how to increase the profitability of the enterprise by 100%.

What is profit

There are several formulas for calculating this financial indicator:

- Revenue - Production cost - Expenses (production, general business, other) - Taxes.

- Financial profit + Gross + Operating - Taxes.

- Profit before tax - Taxes.

Different ways of expression, but the essence is the same.

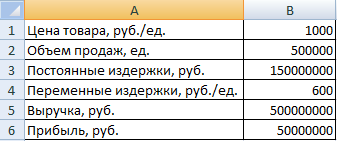

Let's calculate the net profit on the balance sheet using an Excel spreadsheet:

The figures are conditional. This calculation allows you to see what determinants affect the formation of profits.

To obtain net profit, you need to find profit before tax, marginal and operating.

How are these indicators related?

- Gross (marginal) illustrates the effectiveness of sales.

- Profit from sales (operating) shows how productive the main activity is (production efficiency, for example).

- Profit before tax is net of other income and expenses from ancillary activities.

Thus, net profit is an indicator of the efficiency of the enterprise, freed from all costs and expenses.

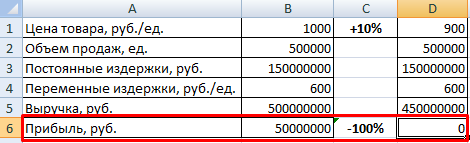

How to increase the profitability of the enterprise by 100%

In essence, three determinants affect the return on investment: the cost of the product, the volume of sales, and the costs (fixed and variable). Let's see how to increase the profitability of the enterprise by influencing one of these factors.

Let's use a simpler table:

The products sold are profitable. The business margin is 10%.

How to change each factor to increase profit by 100% (keeping other conditions):

The leverage effect will be only three. Although it is difficult to reduce fixed costs. You can save on overhead costs (travel, employee training, eliminate losses from downtime, etc.).

Let's try to increase sales by 10%.

Profit only increased by 29% (compared to a 100% increase in profit for a 10% price increase). The leverage effect is three.

To overcome the crisis, the company needs to use all methods to increase profits. Let's look at one more example.

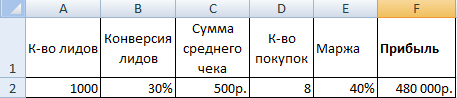

Recall that profit consists of turnover multiplied by margin (formula above). Turnover is the product of three elements: the number of customers, the number of purchases (how many times customers make a purchase in a certain period) and the amount of the average check. Expanding the formula further: the number of customers is the number of potential buyers (leads) multiplied by the conversion of buyers.

Potential buyers are people who have shown interest in the product (went to the store, called the ad, looked at the website). Buyer conversion allows you to find out how many potential buyers became real (made a purchase).

So we came to the detailed profit formula, which was indicated at the beginning of the article:

(Number of leads * Lead conversion) * Average check * Number of purchases * Marginality of the business.

Calculate the company's profit for the previous period:

How to optimize these factors in order to increase the profitability of the enterprise by 100%:

We increased the number of potential buyers by only 15%. Customer conversion - by 5%. The amount of the average check - by 15%. Marginality - by 5%. As a result, profit will increase by 100%.

Thus, by influencing only one of the factors, it is difficult to achieve the necessary improvements. The greatest impact on the profit of investments is the price, the smallest - the volume of sales. A fall in sales will not affect profits as critically as a fall in prices. It is important to avoid the simultaneous reduction of these two indicators by any means.

Variable and fixed costs (together) affect net revenue in much the same way as price. Therefore, the best way to increase profits is to optimize costs and prices.